The new regime was introduced through the Union Budget, 2020. Moreover, it is an optional tax regime which can be opted only by individuals and HUFs.

What is New Regime?

The new regime is a tax regime under Section 115BAC of the Income Tax Act. In addition, this regime gives individuals and HUFs taxpayers an option to pay income tax at lower rates. Furthermore, this regime is applicable from the Financial Year 2020-21 (AY 2021-22).

Note:

In addition, if the person opts for this tax regime, then he will have to forego the majority of the tax exemptions, allowances and deductions. Moreover, on the other hand, if the person chooses to continue with the old tax regime. Furthermore, he can continue to avail all these exemptions, allowances as well as deductions.

Also Read: Major Exemptions & Deductions Availed by Taxpayers in India

Income Tax rates applicable under the New Tax Regime

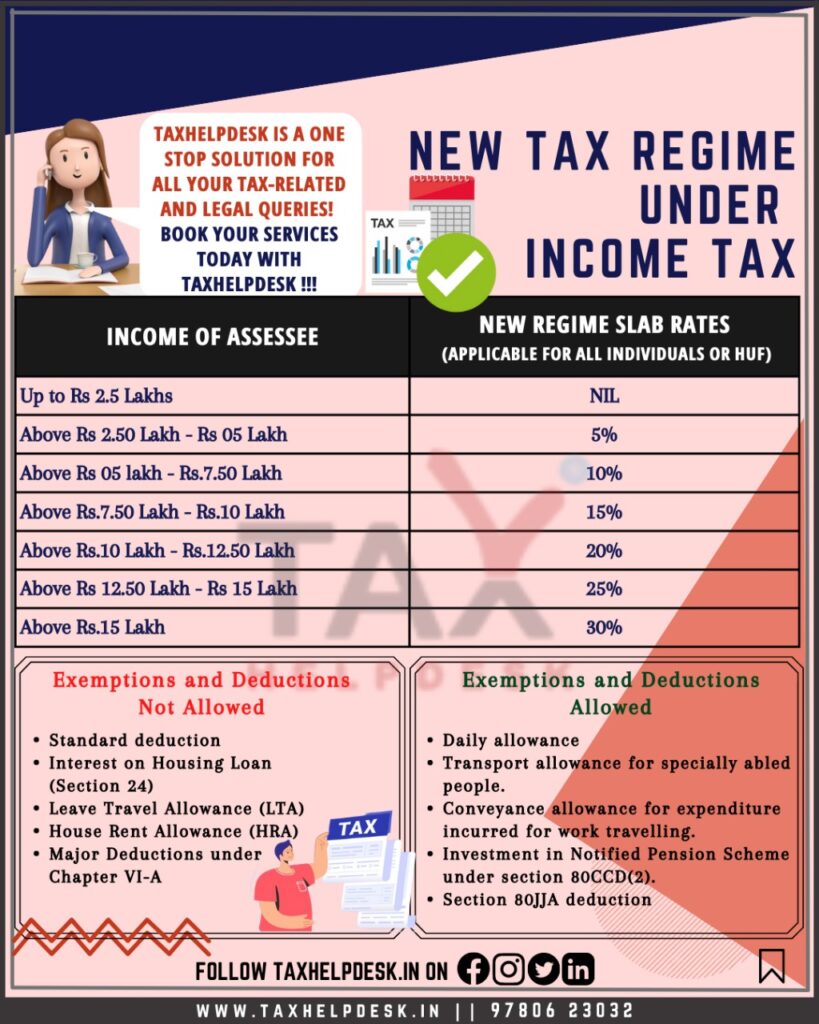

| INCOME | SLAB RATE |

|---|---|

| Up to Rs. 2.5 lacs | NIL |

| Rs. 2.5 lacs – Rs. 5 lacs | 5% |

| Rs. 5 lacs – Rs. 7.5 lacs | 10% |

| Rs. 7.5 lacs – Rs. 10 lacs | 15% |

| Rs. 10 lacs – Rs. 12.5 lacs | 20% |

| Rs. 12.5 lacs – Rs. 15 lacs | 25% |

| Above Rs. 15 lacs | 30% |

List of allowances not available under this Regime

Following are the allowances which are not available under this latest Regime:

– Leave Travel Allowances applicable to individuals with salary

– House Rent Allowance available to salaried individuals

– Helper Allowance

– Academic, research and training pursuits in educational and research institutions allowance

– Uniform allowance

– Special compensatory allowances wrt hilly areas / high altitude area / uncongenial climate area / snow bound area/ avalanche area

– Any special compensatory allowance wrt border area / remote locality / difficult area or disturbed area

– Special compensatory (Tribal Areas / Schedule Areas / Agency Areas) allowance

– Transport allowance, where daily allowance is not available

– Children education allowance

– Children hostel allowance

– Compensatory field area allowance

– Compensatory modified field area allowance

– Counter insurgency allowance available to members of armed forces operating in areas away from their permanent locations

– Underground allowance, which is available to employees who is working in uncongenial, unnatural climate in underground mines

– Special allowance in the nature of high altitude (uncongenial climate) granted to the member of the armed forces operating in high altitude areas

– Any special allowance available to members of armed forces wrt highly active field area

– Island duty allowance

– Allowances available to Member of Parliament or any State Legislature or of any committee. Furthermore, thereof any income by way of daily allowance or any allowance

– In addition, allowance on clubbing of income of minor with parent’s income

Also Read: Which tax regime suits you: Old v. New?

List of deductions not available under New Tax Regime

The list of deductions which are not available under the regime is as follows:

– Standard deduction

– Deduction of entertainment allowance and professional tax

– Interest on housing loan under Section 24(b)

– Deductions under Section 35AD and Section 35CCC

– Major deductions under Chapter VI-A

– Moreover, deduction from family pension

Also Read: Understand about Exemptions & Deductions under New & Old Tax Regimes

Allowances & Deductions available under New Tax Regime

The allowances and deductions which you still can avail under the latest regime are as follows:

Firstly, allowances to meet the cost of tour/travel for employment

Secondly, transport allowance to ‘divyang’ or specially-abled person. In addition, this is to commute between the place of residence and place of work

Thirdly, conveyance allowance for office duties

Fourthly, daily allowance to meet daily charges when working out of the office

Fifthly, deduction on employer’s contribution to National Pension Account [Section 80CCD(2)]

In addition, deduction on additional employee cost [Section 80JJA]

Conditions for availing new Tax regime

While this regime offers lower income tax rates, the individual or HUF. Moreover, this must fulfil the following conditions to be eligible for payment of income tax. In addition, these conditions are as per the new (concessional) income tax slab rates:

- The total income of the individual or HUF should not include business income.

- The calculation of the total income of the individual or the HUF should be without availing the allowable exemption. Furthermore, the deductions under different sections of the Income Tax Act.

- In addition, the calculation of the total income should be without setting off any losses. Moreover, it includes both carry forward and depreciation- losses. Furthermore, there cannot be the deduction of capital losses from the sale of house property from the total income.

FAQs

An individual or HUF can opt for the tax regime at any time before filing the Income Tax Return of the relevant financial year.

You can choose to opt between the two tax regimes at any time before the filing of your Income Tax Return. Moreover, even if you have made a declaration to your employer that you will opt for the old tax regime. Furthermore, also you can choose to file your ITR under the new tax regime.

Salaried individuals and pensioners can switch between new and old tax regimes in the subsequent years. However, taxpayers having business income are not eligible to choose between the new and old tax regimes every year. Moreover, these individuals having business income have only once in a lifetime option. Furthermore, there is need to choose between the two tax regimes.

Disclaimer: The views of the author are personal. TaxHelpdesk owes no responsibility in any manner whatsoever.

Join our Telegram Channel for more updates on Income Tax, GST and finance.