Many people think that the income earned by the minors is not taxable and if they clubbing of income of minor child, then it will lead to reduction of their tax liability. However, as per the provisions of Section 64 of Income Tax Act, if the minor earns any income, then that is clubbed with the income of their parents.

Clubbing of Income, in simple terms means that the income of one person is clubbed in the income of the other person. This clubbing of income can be done with the income of spouse, income of minor child, income from assets transferred to son’s wife/spouse, and so on. Having stated this, the income earned by minor is also taxable under the Income Tax Act.

Also Read: High End Value Transactions Tracked By Income Tax Department

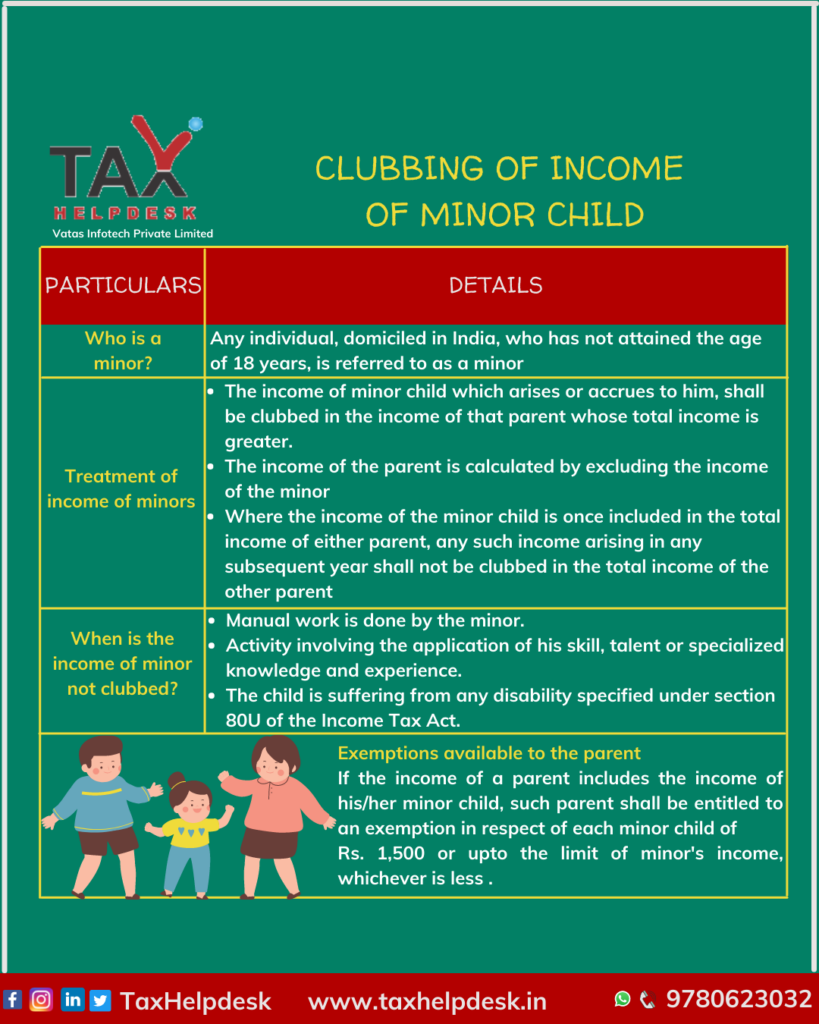

Who is a minor for the purpose of clubbing of income of minor child?

As per the Indian Majority Act, 1875, the age of majority in India is specified as 18 years. Accordingly, any individual, domiciled in India, who has not attained the age of 18 years, is referred to as a minor.

Treatment of income of minors

The income of minor child which arises or accrues to him, shall be clubbed in the income of that parent (mother/father) whose total income is greater.

Note:

– The income of the parent is calculated by excluding the income of the minor child under Section 64(1A) of the Act.

– The child also includes step child and adopted child.

In a case where the income of the minor child is once included in the total income of either parent, any such income arising in any subsequent year shall not be clubbed in the total income of the other parent, unless the A.O. (Assessing Officer) is satisfied, after giving an opportunity of being heard to that parent, that it is necessary so to do.

Illustration:

Taimur is the minor child of Saif and Mrs Kareena. During the previous year 2020-2021, the income of Taimur was Rs. 2,500 and during this previous year, the income of Mrs. Kareena is higher than that of Saif.

As per the provision stated above, the income of Taimur i.e., Rs. 2,500 will be clubbed in the income of Mrs. Kareena for the previous year 2020-2021. In the succeeding years (during the minority of the child), the income of Taimur will be clubbed in the income of Mrs. Kareena, even if the income of Saif becomes higher than that of Mrs. Kareena in any of the subsequent years.

Also Read: Deductions under Section 80C & its allied Sections

However, there is one exception to this clause. If in the succeeding years, the A.O. (Assessing Officer) wants to include the income of the minor child (Taimur) in the hands of Saif, it can be done only if it is necessary to do so (not merely in the change in opinion of the Assessing Officer) and that too after giving an opportunity of being heard to Saif.

Cases where the income of minor will not be clubbed with his/her parents income

Clubbing of income of minor child with the income of his/her parents shall not be done, in following cases:

a) Income of a disabled child (disability of the nature specified in section 80U)

b) Income earned by manual work done by the child or by activity involving application of his skill and talent or specialised knowledge and experience

c) Also, money gifted to an adult child is exempt from gift tax under gifts to ‘relative’.

Illustration 2

Mrs Sonia has two minor children, viz., Rahul and Priyanka. Rahul is a child artist and Priyanka is suffering from diseases specified under section 80U of the Income Tax Act. Income of Rahul and Priyanka are as follows:

Income of Rahul from stage shows: Rs. 1,00,000

Income of Rahul from fixed deposits invested by Mrs. Sonia: Rs. 6,000

Income of Priyanka from fixed deposits invested by Mrs. Sonia: Rs. 1,20,000.

Will the income of minor children be clubbed with the income of their parent (Mrs. Sonia is not having any income)?

| Particulars | Whether income will be clubbed or not? | Reasons |

|---|---|---|

| Income from stage shows of Rs. 10,00,000 of Rahul | No | Income is earned through activity involving the application of his skill, talent or specialized knowledge and experience. Therefore, income will not be clubbed |

| Income of Rahul from fixed deposits invested by Mrs. Sonia of Rs. 6,000 | Yes | Amount invested in Fixed Deposits by parent in the name of minor child |

| Income of Priyanka from fixed deposits of Rs. 12,00,000 invested by Mrs. Sonia | No | Priyanka is a minor suffering from disability specified under section 80U. Therefore, income will not be clubbed. |

FAQs

If the marriage of the parents does not subsist, then the income of minor child will be included in the income of that parent (mother/father) who has maintained the minor child (guardian of the minor child) in the relevant previous year.

Also Read: Income Tax Slab Rates For Individuals Under The Old And New Tax RegimeWhere both the parents of the minor child are not alive, the income of the minor child cannot be assessed in the hands of any other relatives (including grandparents) or even in the hands of a minor.

The income of minor will not be clubbed with the income of his parent and will be treated as a part of his income in the following cases:

– Income earned through activity involving the application of his skill, talent or specialized knowledge and experience – Income is earned by a child suffering with specified disability defined in Section 80U of the Income Tax Act. – Income earned by minor is through some manual work done by him. Illustration: Mrs Sonia has two minor children, viz., Rahul and Priyanka. Rahul is a child artist and Priyanka is suffering from diseases specified under section 80U of the Income Tax Act. Income of Rahul and Priyanka are as follows: Income of Rahul from stage shows: Rs. 1,00,000 Income of Rahul from fixed deposits invested by Mrs. Sonia: Rs. 6,000 Income of Priyanka from fixed deposits invested by Mrs. Sonia: Rs. 1,20,000.As per Section 64(1A) of the Income Tax Act, where the income of an individual also contains the income of his/her minor child, such individual shall be entitled to an exemption of Rs. 1,500 in respect of each minor child.

However, where the income of any minor is less than Rs. 1500, then the aforesaid exemption shall be restricted to the income so included in the total income of the individual.

If you have any suggestions/feedback, then please drop us a message in the chat box. For more updates on Taxation, Financial and Legal matters, join our group on WhatsApp, channel on Telegram or follow us on Facebook, Instagram, Twitter and Linkedin!

The views of the author are personal. TaxHelpdesk does not owe any responsibility!

Pingback: Clubbing of Income of Husband And Wife | TaxHelpdesk

Pingback: Clubbing of Income of Husband & Wife | TaxHelpdesk

Pingback: All about Advance Tax under Income Tax Act | TaxHelpdesk

Pingback: Know about Clubbing of Income of Husband & Wife | TaxHelpdesk