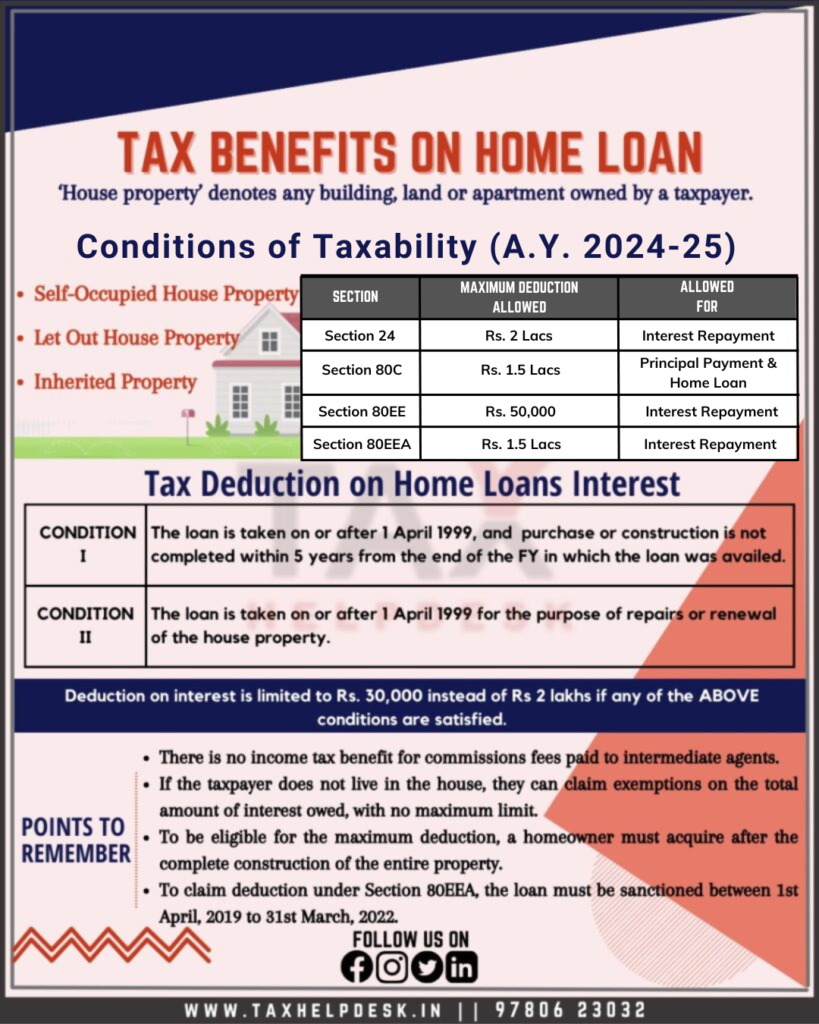

On purchase of residential property through a home loan, one can save taxes through Section 24, Section 80C, Section 80EE and Section 80EEA of the Income Tax Act.

Time and again we keep getting queries that how can we save taxes on the purchase of residential property through a home loan. Therefore, we have come up with this blog that explains in detail the tax-saving schemes wrt the purchase of residential property through a home loan.

On purchase of residential property through a home loan, one can save taxes through Section 24, Section 80C, Section 80EE, and Section 80EEA of the Income Tax Act for the Assessment Year 2024-25. The claiming of deductions under these Sections can be either on the principal amount or the interest amount.

Who can claim deduction on home loan?

The provision of the Income Tax Act clearly states that only that person can claim the deduction on a home loan who has title over the property as well as has taken a loan in his name. In other words, the person must be:

– Owner of the property, and

– Borrower of the loan

Note:

The deduction on the home loan is available only to the individuals or members of HUFs and not to any other person. Therefore, companies, partnership firms, body corporates, or trusts cannot claim deductions on home loans.

Also Read: 10 Best Ways to Save Taxes in 2022!

Now, let us know each provision in detail

Section 24: Deductions from income from House Property

As per the provisions of Section 24, if a person takes a home loan for purchase or construction, then whatever interest he pays on the principal amount of the loan is free from paying taxes.

Also Read: A Quick Look At Deductions Under Section 80C To Section 80U

The sub-clauses in this category are:

- If the loan has been taken for a self-occupied property, then he can claim a deduction of up to Rs. 2 lakh or the amount of loan, whichever is lower.

- If the loan is for the purchase or construction (not renovation) of a property before actually buying or completing its construction, then also the person can claim the interest.

- And, the claiming of deductions can be on the payment of interest before the completion of construction or purchase, in 5 equal installments, from the year of purchase of the house or the completion of the construction.

To avail of this deduction, the person needs to compute the interest amount he has to pay to the bank or financial institution from where he has taken the loan and separate it from the principal repayment. Moreover, it does not matter whether there is actual payment of amount to the financier – one can get the deduction for the complete annual interest amount.

Also Read: Do I need to file Income Tax Return?

Conditions for claiming deduction under Section 24

- Firstly, the person has to buy or complete construction of the house within 5 years (3 years till FY 2015-2016) of taking the loan for him to be able to claim maximum deduction on the loan interest amount.

- Secondly, the home loan date is on or after 1st April, 1999

- Lastly, the person must have an interest certificate for the loan that he is taking.

Certain Exceptions to Section 24

- If there is no occupancy of the house by person because he lives in another town due to employment or business, and lives in another property or on rent in the city of his employment, then he can claim tax deduction on interest payment only up to Rs. 2 lakh.

- There is no deduction for any brokerage or commission for arranging the loan or tenant.

Section 80C: Home Loan Deduction on Principal Amount

Section 80C allows deduction on payment of the principal amount for the relevant financial year. Further, the amount of deduction available under Section 80C is the principal amount or Rs. 1,50,000, whichever is lower.

Also Read: Understand About Taxability Of Various Investments Under Section 80C

Section 80C deductions conditions

There is only one condition under Section 80C for claiming deductions on the home loan – that there should be no selling of the house within 5 years of possession.

Note:

If the property is sold within 5 years of possession, then the deduction which has been claimed earlier shall be added back in the income of the person in the year of sale.

Apart from the above deduction, the person can also claim the deductions for stamp duty and registration fees under Section 80C. However, it is subject to the bracket of Rs. 1.5 lacs. Further, one can claim these expenses only in the actual year of incurring of these expenses.

Section 80EE: Deduction on interest on home loan

In addition to the above deductions, Section 80EE provides deduction in respect of interest on loans for residential house property. The maximum allowable deduction under this Section is Rs. 50,000/-

Also Read: Major Exemptions & Deductions Availed By Taxpayers in India

Deduction Conditions under Sections 80EE

- The amount of the loan should be Rs 35 lakhs or less.

- The value of the property should not exceed Rs 50 lakhs.

- The date of sanction of loan must be between 1st April 2016 to 31st March 2017.

- On the date of sanction of loan, the individual should not own any other house. In other words, he should be first-time house owner.

Section 80EEA: Deduction on Home Loan for Certain House Property

The provision Section 80EEA was introduced by the Union Budget, 2019. Consequently, it allows deduction in respect of interest on loans for certain house property. Further, it allows a maximum deduction of upto Rs. 1,50,000.

Also Read: Know Taxability of Capital Assets in India

Conditions for Section 80EEA

- The stamp value of the property should not exceed Rs 45 lakhs.

- The date of sanction of the loan must be between 1 April, 2019 to 31 March, 2020.

- On the date of sanction of loan, the individual does not own any other house i.e., he must be first-time home buyer.

- The individual should not also be eligible to claim deduction under section 80EE.

Brownie Point: Deduction for Joint Home Loan

If the loan is a joint home loan, then each of the loan holders can claim a deduction for home loan interest up to Rs 2 lakh each under Section 24 and principal repayment under Section 80C up to Rs 1.5 lakh each in their individual Income Tax Returns.

Condition for claiming deduction on joint home loan

To claim deduction on the joint home loan, the persons should also be co-owners of the property taken on loan.

Note:

Joint Home Loan can be taken by any two persons who are major and are of sound mind. Additionally, there is no requirement that a joint home loan can only be taken by the members of the family.

FAQs

If the completion of construction or purchase is not within 5 years, then person will be able to claim only Rs. 30,000 (standard deduction) under Section 24(a) and not Rs. 2 lac (maximum benefit) under Section 24(b).

No, these deductions are available only under the old tax regime.

If you want to know more about tax deduction on home loan or take TaxHelpdesk’s experts consultation, then drop a message below in the comment box or DM us on Whatsapp, Facebook, Instagram, LinkedIn and Twitter. For more updates on tax, financial and legal matters, join our group on WhatsApp and Telegram!

Disclaimer: The views are personal of the author and TaxHelpdesk shall not be held liable for any matter whatsoever!

Pingback: Know About Systematic Investment Plan (SIP) | TaxHelpdesk