Deductions under Section 80C to Section 80U are covered under Chapter VIA of the Income Tax Act. The quantum of the deduction varies from Section to Section and type of person.

A lot many individuals find the current taxation system as difficult to comprehend. The taxation rates for individuals are based on the income earned by an individual and his residential status. The Government of India, has over the years by way of amendments in the Finance Act provided taxpayers in India with more than 70 exemptions as well as deductions options through which the individuals can bring their taxation liability. In this blog, we will discuss in detail the deductions under Section 80C to Section 80U

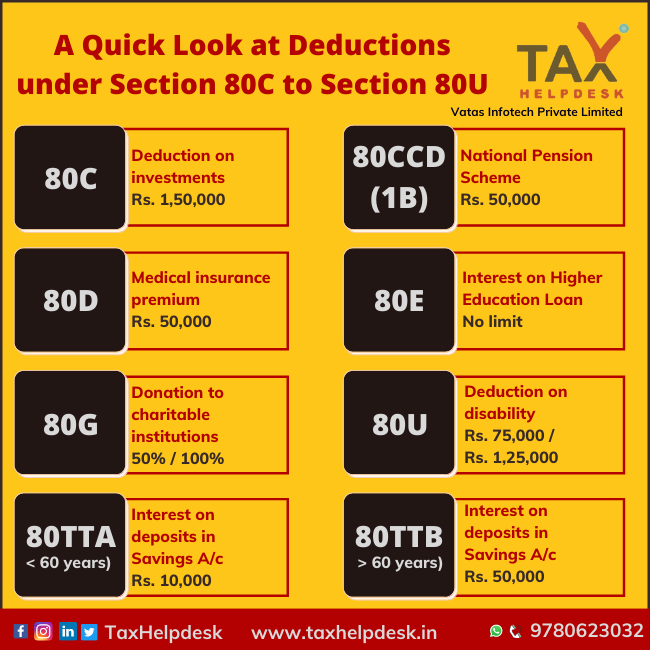

List of Deductions under Section 80C to 80U

| Section | Deduction Description | Maximum Limit |

|---|---|---|

| 80C | Deduction for investments in specified financial instruments | Rs. 1,50,000 per annum |

| 80CCC | Deduction for contributions to pension funds | Rs. 1,50,000 per annum |

| 80CCD(1) | Deduction for contributions to the National Pension Scheme | Up to 10% of salary |

| 80CCD(1B) | Additional deduction for contributions to NPS | Rs. 50,000 per annum |

| 80CCD(2) | Deduction for employer’s contribution to NPS | Up to 10% of salary |

| Section 80CCH | Contributions to Agniveer Corpus Fund | Entire amount that has been contributed |

| 80D | Deduction for medical insurance premiums |

Up to Rs. 50,000 per annum (for senior citizens), Up to Rs. 25,000 per annum (for individuals below 60 years) |

| 80DD | Deduction for expenses on medical treatment of disabled dependents | Rs. 75,000 to Rs. 1,25,000 (depending on the disability) |

| 80DDB | Deduction for medical treatment of specified diseases | Rs. 40,000 to Rs. 1,00,000 (depending on the age and disease) |

| 80E | Deduction for interest on education loan | No maximum limit |

| 80EE | Deduction for interest on home loan for first-time homebuyers | Up to Rs. 50,000 per annum |

| 80G | Deduction for donations to certain funds, charities, etc. | 100% or 50% of the donated amount (subject to limits) |

| 80GG | Deduction for rent paid when HRA is not received | Least of: Rs. 60,000 per annum or 25% of total income |

| 80GGA | Deduction for donations to scientific research or rural development | 100% of the donated amount |

| 80GGB | Deduction for contributions to political parties (by companies) | 100% of the donated amount |

| 80GGC | Deduction for contributions to political parties (by individuals) | 100% of the donated amount |

| 80IA | Deduction for profits and gains from certain industrial undertakings | 100% or 30% of profits (subject to conditions) |

| 80IAB | Deduction for profits and gains from certain startups | 100% of profits (subject to conditions) |

| 80IB | Deduction for profits and gains from certain businesses | 100% or 30% of profits (subject to conditions) |

| 80IC | Deduction for profits and gains from certain enterprises | 100% or 30% of profits (subject to conditions) |

| 80ID | Deduction for profits and gains from certain industries | 100% or 30% of profits (subject to conditions) |

| 80IE | Deduction for profits and gains from certain undertakings | 100% or 30% of profits (subject to conditions) |

| 80JJA | Deduction for profits and gains from certain employment | 100% of additional employee cost |

| 80JJAA | Deduction for employment of new employees | 30% of additional employee cost |

| 80JJAB | Deduction for employment of new employees (in specified industries) | 100% of additional employee cost |

| 80LA | Deduction for certain incomes of offshore banking units | 100% of specified income |

| 80P | Deduction for income of co-operative societies | As per provisions of the section |

| 80QQB | Deduction for royalty income of authors, playwrights, etc. | Rs. 3,00,000 per annum |

| 80RRB | Deduction for income from patents | Rs. 3,00,000 per annum |

| 80TTA | Deduction for interest on savings bank accounts | Up to Rs. 10,000 per annum |

| 80TTB | Deduction for interest income for senior citizens | Up to Rs. 50,000 per annum |

| 80U | Deduction for individuals with disability | Rs. 75,000 to Rs. 1,25,000 (depending on the disability) |

deductions under Section 80C to Section 80U under the tax regimes

All the deductions under Section 80C to 80U are not available under both the tax regimes. That is to say, only deductions under Section 80CD(2) and Section 80JJA are available under the new tax regime. Whereas, under the old tax regime, all the deductions under Section 80C to 80U are available to the person eligible to claim them.

Also Read: Which tax regime suits you: Old v. New?

Let us discuss in detail all of these deductions.

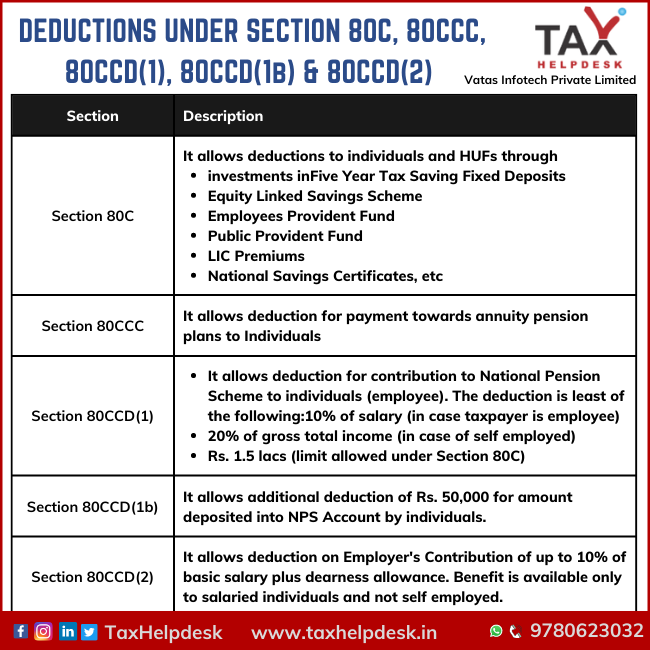

Section 80C: Deduction in respect of investments

The deductions under Section 80C are the most popular deductions among the taxpayers. This is so, because it allows the person to reduce his taxable income by making investments in tax saving instruments. Further, only individuals and HUFs can claim deduction under Section 80C. On the other hand, companies, partnership firms and LLPs cannot claim deduction under Section 80C. In addition to this, the deduction limit under Section 80C is Rs. 1.5 lacs.

Also Read: Best Ways to Save Taxes (other than Section 80C)

Note:

Section 80C includes subsections , 80CCC, 80CCD (1) , 80CCD (1b) and 80CCD (2). The bifurcation of the deductions available under these Sections are as follows:

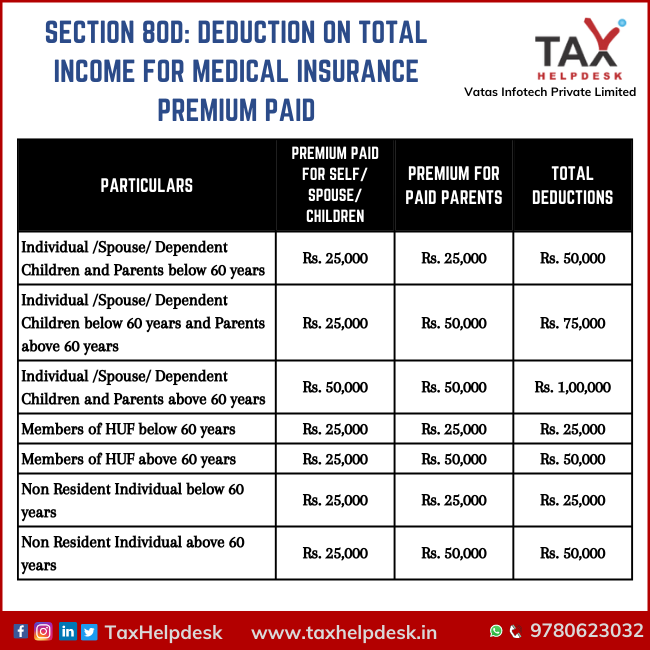

Medical Insurance Deduction: Section 80D

A person being individual or HUF can claim the deduction in respect of health insurance premium under Section 80D. Under this deduction, the person can claim the following tax benefits:

– Firstly, medical insurance premiums

– Secondly, expenditure on preventive health check-ups

– Lastly, other medical expenditures.

Also Read: Know About Health Insurance Tax Benefits Under Section 80D

The bifurcation of deductions available under Section 80D is as follows:

Specified diseases treatment: Deduction under Section 80DDB

In addition to the deduction in respect of health insurance premiums under Section 80D, there is another deduction available under Section 80DDB. This section allows a deduction on the treatment of severe disease of the individual or his dependent. Further, the maximum amount of deduction that a person can claim under Section 80DDB is

– Rs. 40,000, in case assessee is below the age of 60 years

– Rs. 1,00,000 in case assessee is above the age of 60 years.

Also Read: Section 194D: TDS On Insurance Commission

Income Tax Deduction for medical treatment of dependent with disability: Section 80DD

To provide financial aid to persons with disability, the Income Tax Act provides a deduction under Section 80DD. Further, the quantum of the deduction depends upon the percentage of the disability, which is as follows:

– Disability is more than 40% but less than 80%: Rs. 75,000

– Disability is more than 80%: Rs. 1,25,000

Also Read: Best Ways to Save Taxes in 2023!

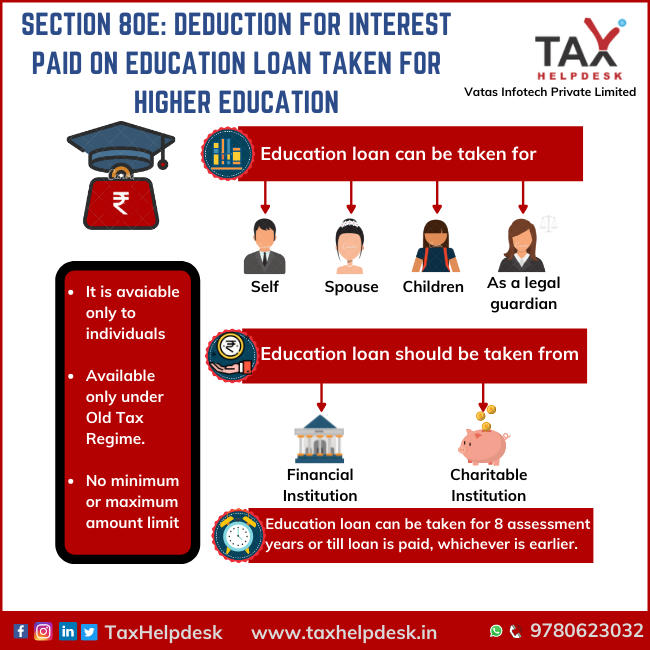

Section 80E: Deduction for interest paid on higher education loan

The Income Tax Act allows a deduction for interest paid on higher education loans under Section 80E. In order to claim the deduction under this Section, the loan must be either for the taxpayer or his spouse or his children or for a student for whom he is a legal guardian.

Also Read: Documents to be submitted to employer to claim tax benefits

Please note that the deduction under Section 80E is available for a maximum period of 8 years (beginning the year in which the interest starts getting repaid) or till the entire interest is repaid, whichever is earlier. However, there is no restriction on the amount that can be claimed.

Interest on Home loan deduction under Section 80EE

Section 80EE allows deduction to individuals on interest on home loan for up to Rs. 50,000. However, this deduction is available to an individual only if he satisfies the following conditions:

– He should own only one house property on the date of sanction of the loan

– The value of the property must be less than Rs. 50 lacs

– The home loan value must less than Rs. 35 lacs

– The date of sanction of loan must be between 1st April, 2016 to 31st March, 2017

– The loan must be sanctioned by a financial institution or housing finance company.

In addition to the above, there was an introduction of new section – Section 80EEA through Union Budget 2019. This new Section allows an interest deduction of up to Rs. 1,50,000 for housing loans taken for affordable housing during the period 1 April 2019 to 31 March 2020.

Also Read: Tax Benefits On Home Loan: Know More At TaxHelpdesk

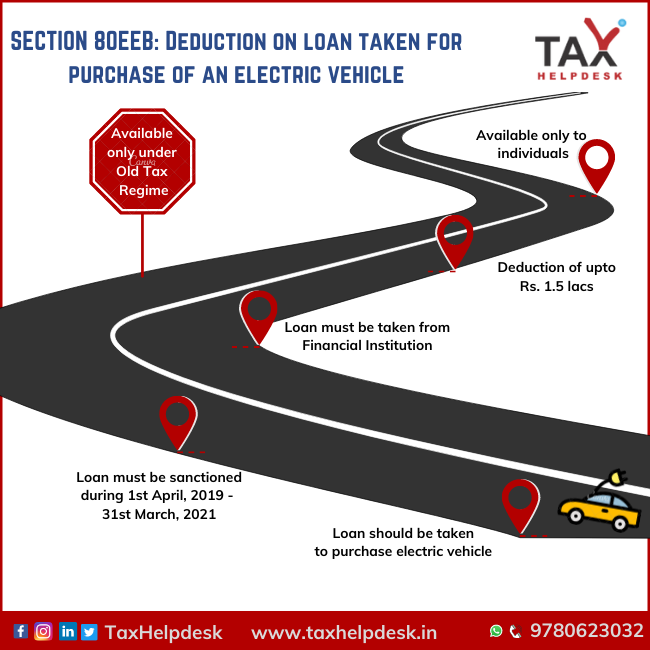

Deduction on interest paid on loan taken for purchase of electric vehicle: Section 80EEB

Section 80EEB allows a deduction of up to Rs. 1,50,000 in respect of payment of interest on the loan of the electric vehicle. This deduction can be claimed only by individuals and not by any other person. In order to claim deduction under this Section, the following conditions must be fulfilled:

– The loan must be taken from a financial institution or NBFC for buying an electrical vehicle

– The date of sanction of the loan must be between 1st April, 2019 to 31st March, 2023.

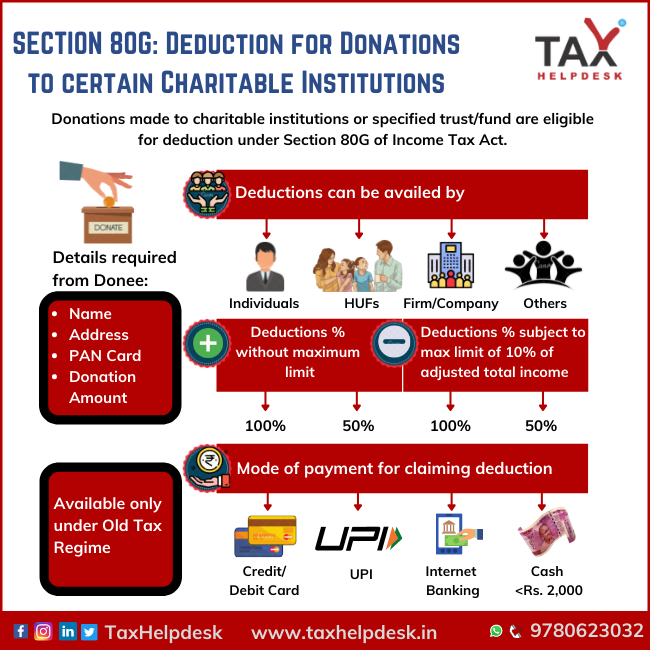

Donation to Charitable Institutions: Section 80G

Individuals, HUFs as well as businesses can claim deductions on donations paid to certain relief funds and charitable institutions. Further, please note that not all donations are eligible for deduction under Section 80G. That is to say, the person can claim deductions only on funds prescribed by the government of India that qualify as a deduction.

Also Read: Deduction on Donation to Charitable Institutions

Additionally, the qualifying limits of the deduction vary on the type of charitable institution. The same is as follows:

– 100% Income Tax Deduction without any qualifying limit

– 50% Income Tax Deduction without any qualifying limit

– 100% Income Tax Deduction subject to 10% of adjusted gross total income

– 50% Income Tax Deduction subject to 10% of adjusted gross total income

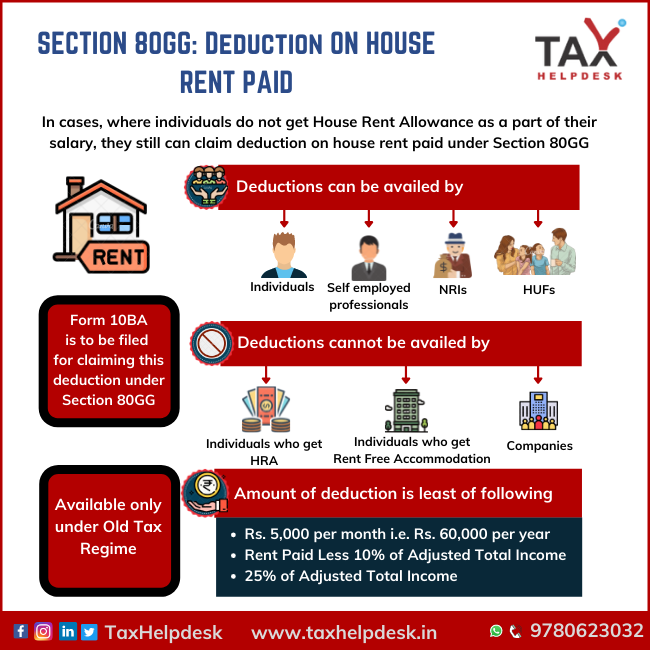

Deduction on house rent paid: Section 80GG

Individuals who do not receive House Rent Allowance from their employers can claim the deduction under Section 80GG. This deduction is available on rent payments where HRA is not available. Further, to claim deduction under Section 80GG, there must be a fulfilment of the following conditions:

– The taxpayer, spouse or minor child should not own residential accommodation at the place of employment

– He should not have self-occupied residential property in any other place

– He must be living on rent and paying rent

Contributions to political parties: Deduction under Section 80GGB & Section 80GGC

The contributions made by companies or any persons to political parties are eligible for tax deduction under Section 80GGB & Section 80GGC respectively. However, in order to claim the deduction under these Sections, the contribution must be made through any mode other than cash. Furthermore, there is no maximum limit applicable on contributions made to political parties.

Also Read: TDS on cash withdrawal from bank

Royalty on Patents: Deduction under Section 80RRB

An author (Resident of India or resident but not ordinarily resident in India), including the joint author of a book, can claim a deduction under Section 80QQB. The deduction amount shall be as follows:

a. In the case of lump sum payment – Total amount of royalty income subject to a maximum of Rs. 3,00,000.

b. In other cases – Total amount of such income subject to a maximum of 15% of the value of books sold during the previous year.

Interest on deposits in Savings Account: Section 80TTA & Section 80TTB

Section 80TTA and Section 80TTB allow deduction on interest on deposits in the savings account. Section 80TTA, provides a deduction of up to Rs. 10,000 to individuals up to the age of 60 years. On the other hand, Section 80TTB provides a deduction of up to Rs. 50,000 to individuals above the age of 60 years.

Also Read: Major Exemptions & Deductions Availed by Taxpayers in India

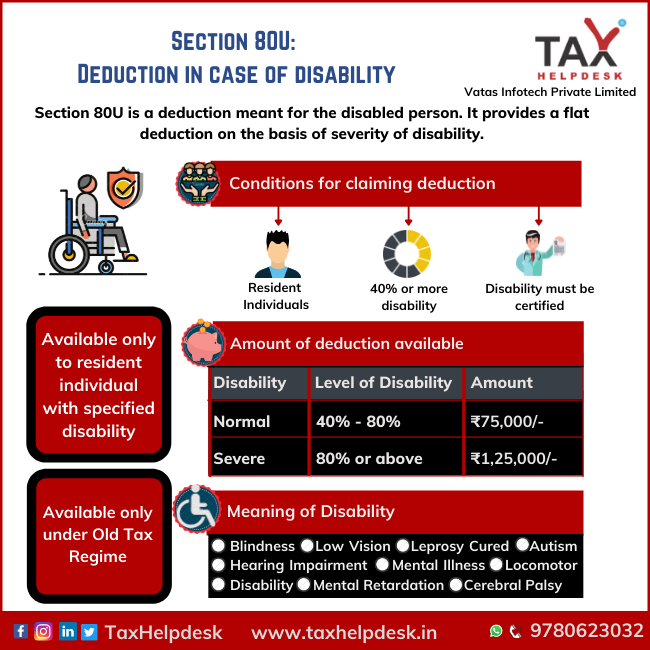

Disabled Individuals deduction under Section 80U

A resident individual certified by the medical authority or a government doctor to be a person with a disability (having a disability of 40% or more) can claim a deduction of Rs. 75,000 under this section. On the other hand, in the case of a person with a severe disability (having a disability of 80% or more ), the quantum of deduction allowed is Rs. 1,25,000. It is a fixed deduction and is not dependent on the actual expenses and age of the person.

Also Read: Section 80U: Deduction In Case Of Disability

If you still have doubts regarding deductions, then drop a message below in the comment box or DM us on Whatsapp, Facebook, Instagram, LinkedIn and Twitter. For more updates on tax, financial and legal matters, join our group on WhatsApp and Telegram!

Disclaimer: The views are personal of the author and TaxHelpdesk shall not be held liable for any matter whatsoever!