The ITC on bank charges can be claimed only if it is in furtherance of business. However, there are certain conditions which needs to be fulfilled for availing input tax credit.

Conditions for availing ITC on bank charges.

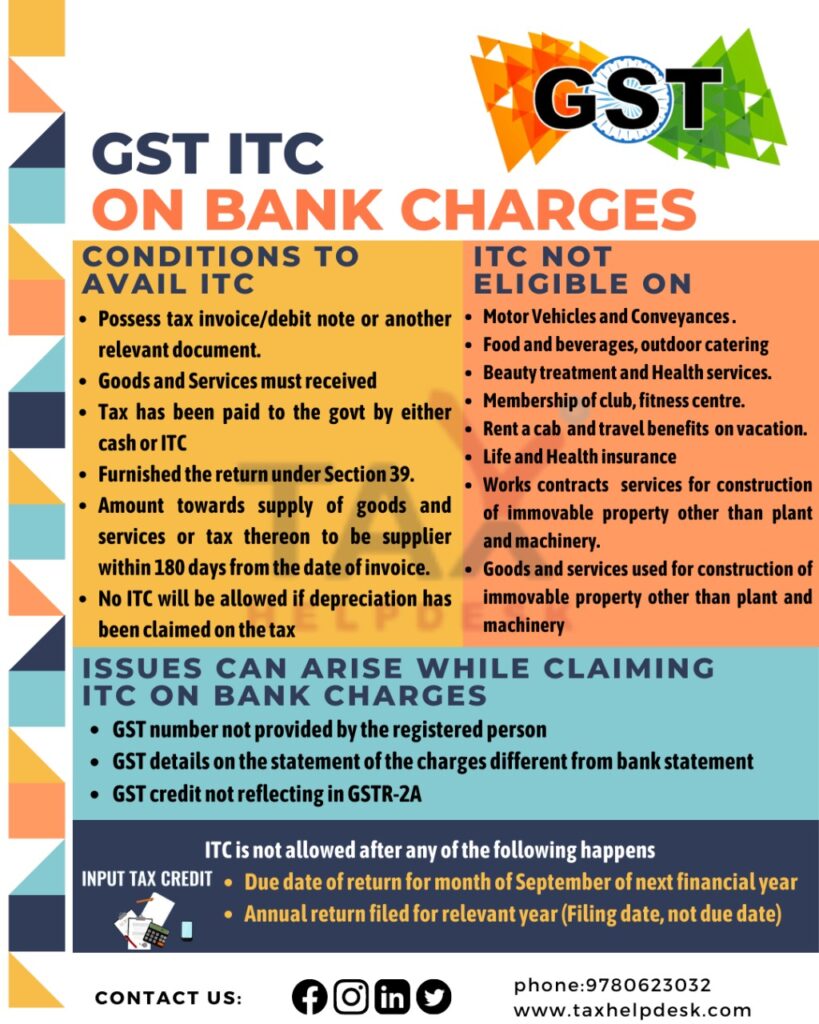

For availing ITC on bank charges, there are 4 four conditions:

– The person must possess tax invoice/debit note or any other document

– The goods or services are received by the person

– The GST has been paid to the government by either cash or ITC

– The person has furnished GST Return under Section 39.

Also Read: How Does Input Tax Credit Work?

Time limit for claiming GST Input Tax Credit

The time limit for claiming goods and services tax input tax credit is

– The date of furnishing of annual return, or

– The return for the month of September following the end of financial year.

To do list for claiming ITC on bank charges

In order to claim ITC on bank charges, the person must go through this checklist:

- Follow the law closely to determine the ITC that is eligible. Special attention needs to be paid to the items on which ITC is blocked by the law itself. Such ITC should not be availed in the first place. Having stated that, GST ITC on bank charges does not come under blocked list.

- Conduct ITC reconciliations i.e., GSTR 2A vs GSTR 3B, GSTR 3B vs purchase register, etc. This activity should be done monthly.

- Check if all vendor payments are made within 180 days or not. In case the vendor payments get spilt beyond 180 days, the ITC needs to be reversed along with interest as applicable.

- Check if ITC availed is only in respect of business supplies and taxable supplies. Any ITC that pertains to exempt or non-business should be reversed.

- Review the ITC in respect of payments made under the reverse charge mechanism.

- In the case of multiple state-wise registrations of the same entity, if ITC is received at a common head office, such ITC needs to be distributed to the relevant GSTINs.

- Most organizations do not avail ITC of bank charges; however, it may be noted that no such restrictions have been prescribed by the law.

- In the case of taxpayers who have taxable supplies of more than INR 50 lakhs, the applicability of Rule 86B needs to be checked.

- Applicability of Rule 36(4) and availability of credit needs to be ascertained on a monthly basis.

- Check if ITC has been restricted by any rate notifications.

Issues that can arise for claiming GST input tax credit

Issues that can arise for claiming GST input tax credit are as follows:

– GST number not provided by the registered person

If the GST number or GSTIN is not provided by the registered person, then bank considers it as B2C (Business to Customer) transaction. However, in order to claim goods and services tax (GST) input tax credit on bank charges, it must be a B2B (Business to Business) transaction.

Also Read: Rules related to setting off of Input Tax Credit

– GST details on Statement of Charges is different from charges in Bank Statement

If there is a mismatch in details of statement of charges and charges in bank statement, then it will lead to problem in GST ITC on bank charges. In case of ambiguity, however, bank statement is to be seen.

-GST credit not reflecting in GSTR-2A

If the GST credit is not reflected in GSTR-2A, then also no ITC on bank charges can be availed. This can be corrected through intimating the bank with date of charge and transaction details.

If you want to know more about GST or take TaxHelpdesk’s experts consultation, then drop a message below in the comment box or DM us on Whatsapp, Facebook, Instagram, LinkedIn and X (Formerly Twitter). For more updates on tax, financial and legal matters, join our group on WhatsApp and Telegram!

Disclaimer: The views are personal of the author and TaxHelpdesk shall not be held liable for any matter whatsoever!