Debit note under GST is a business/formal document used by the seller to remind the buyer of his current debt obligations, or a document produced by a buyer when returning goods purchased on loan.

Meaning of debit note

When a tax invoice has been issued for supply of any goods or services or both and the taxable value or tax charged in that tax invoice is found to be less than the taxable value or tax payable in respect of such supply, the registered person, who has supplied such goods or services or both, shall issue to the recipient a debit note containing the prescribed particulars.

Also Read: GST Registration on the basis of State & Turnover

Who can issue Debit Note

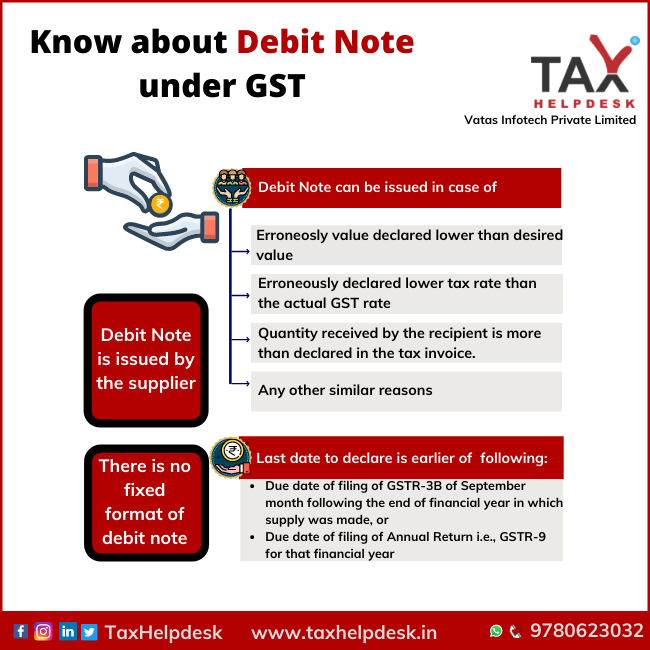

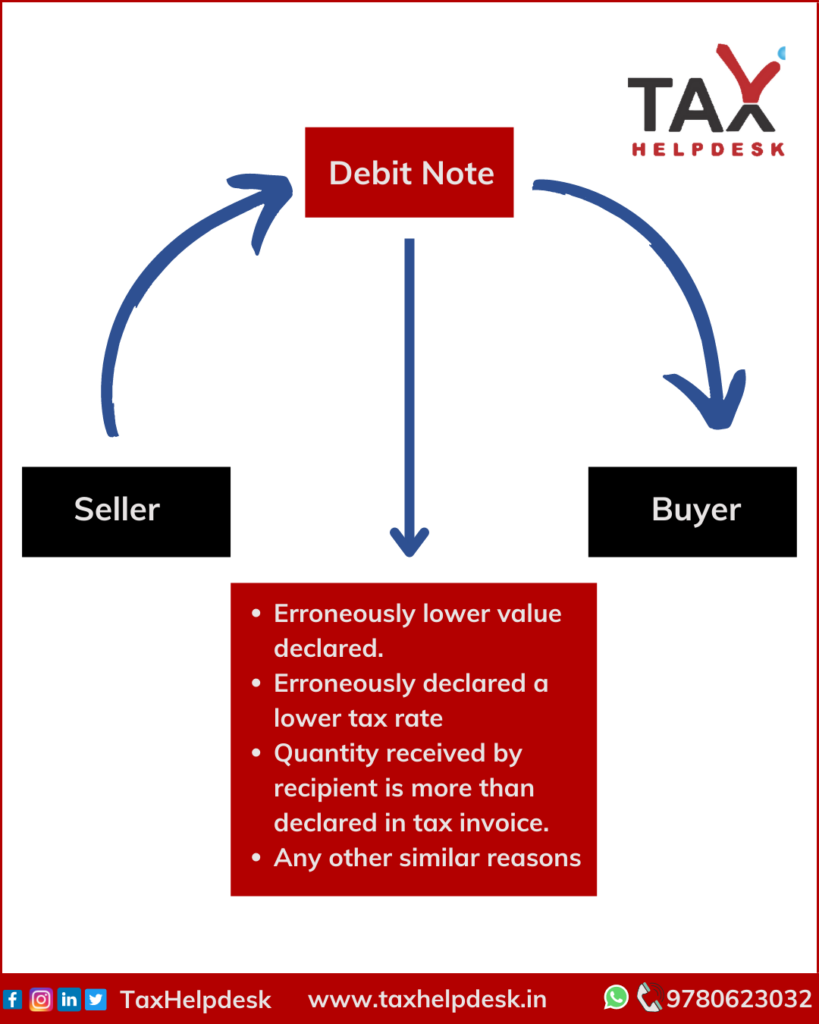

Just like Credit Note, Debit Note also can be issued only by the supplier.

Cases where Debit Note can be issued

The cases where debit note can be issued are:

-The seller has erroneously declared a value less than the actual value of goods or services or both provided.

– The seller has erroneously declared a lower tax rate than what is applicable for the kind of the goods or services or both supplied.

– The quantity received by the buyer/recipient is more than what has been declared in the tax invoice.

– Any other similar reasons.

Illustration

Value of the goods is less than desired value.

| Particulars | Amount |

|---|---|

|

Price at which units are sold (Rs. 10 x 10,000) |

Rs. 1,00,000 |

| GST @5% | Rs. 5,000 |

| Invoice Amount | Rs. 1,05,000 |

| Desired Value of the units | Rs. 12/unit |

|

Debit Note Amount (Rs. 2 x 10,000) |

Rs. 20,000 |

| GST @5% | Rs. 1,000 |

| Total Debit Note | Rs. 21,000 |

GST Rate charged is less than actual GST Rate

| Particulars | Amount/GST Rate |

|---|---|

|

Price at which units are sold (Rs. 10 x 10,000) |

Rs. 1,00,000 |

| GST @5% | Rs. 5,000 |

| Invoice Amount | Rs. 1,05,000 |

| Desired GST Rate | 12% |

|

Debit Note Amount (Rs. 1,00,000 x 12%) |

Rs. 12,000 |

| (-) GST @5% x Rs. 1,00,000 | Rs. 5,000 |

| Total Debit Note | Rs. 7,000 |

Quantity received by buyer is more than desired

| Particulars | Amount/Units |

|---|---|

|

Price at which units are sold (Rs. 10 x 10,000) |

Rs. 1,00,000 |

| GST @5% | Rs. 5,000 |

| Invoice Amount | Rs. 1,05,000 |

| No. of units desired | 5,000 |

|

Debit Note Amount (Rs. 50,000 + 5% GST) |

Rs. 52,500 |

| Units sent | Rs. 1,05,000 |

| Total Debit Note | Rs. 52,500 |

Format Of Debit Note

There is no prescribed format but debit note issued by a supplier must contain the following particulars, namely:

(a) name, address and Goods and Services Tax Identification Number of the supplier;

(b) nature of the document;

(c) a consecutive serial number not exceeding sixteen characters, in one or multiple series, containing alphabets or numerals or special characters hyphen or dash and slash symbolised as “-” and “/” respectively, and any combination thereof, unique for a financial year;

(d) date of issue;

(e) name, address and Goods and Services Tax Identification Number or Unique Identity Number, if registered, of the recipient;

(f) name and address of the recipient and the address of delivery, along with the name of State and its code, if such recipient is un-registered;

(g) serial number and date of the corresponding tax invoice or, as the case may be, bill of supply;

(h) value of taxable supply of goods or services, rate of tax and the amount of the tax debited to the recipient; and

(i) signature or digital signature of the supplier or his authorized representative.

Also Read: Qualifications for GST Registration

Tax liability

The issuance of a debit note or a supplementary invoice creates additional tax liability. The treatment of a debit note or a supplementary invoice would be identical to the treatment of a tax invoice as far as returns and payment are concerned.

In order to claim Input Tax Credit, the debit note must be issued on earlier of the following:

– Due date of filing of GSTR-3B of September month following the end of financial year in which supply was made, or

– Due date of filing of Annual Return i.e., GSTR-9 for that financial year

FAQs

Yes, there is a requirement to maintain record of debit note. The records of the debit note or a supplementary invoice have to be retained until the expiry of seventy two months from the due date of furnishing of annual return for the year pertaining to such accounts and records. Where such accounts and documents are maintained manually, it should be kept at every related place of business mentioned in the certificate of registration and shall be accessible at every related place of business where such accounts and documents are maintained digitally.

If you want to know more about debit note or take help of TaxHelpdesk experts, then leave a message below in the comment box or drop us a message on any of these platforms: WhatsApp, Facebook, Instagram, LinkedIn and Twitter. For tax related information and updates, you can also join our WhatsApp group and Telegram Channel.

The views of the author are persona and Taxhelpdesk does not owe any liability.