The Government puts cash payment restrictions to collect more taxes as well as avoid tax evasion.

For any country to develop and progress, the government needs funds. Consequently, the collection of these funds by the Government can be through various ways and one such way is through imposing taxes on the income of the persons if it exceeds a certain limit of cash transactions. Therefore, by doing so, the Government is not only able to collect the taxes but also stop tax evasions.

Furthermore, to evade income tax, various persons make their transactions through cash and do not report them while ITR filing in India. To curb these practices, the government has put cash payment restrictions on transactions under the Income Tax Act. In addition to this, the government also imposes penalties over and above a predefined threshold limit.

Cash Payment Restrictions under income tax

1. Donations Via Cash Transactions Received By Political Parties (Section 13A)

A political party for the purpose of Section 13A means a political party whose registration is under Section 29A of the Representation of the People Act, 1951. Further, these political parties cannot involve in any activity of a commercial nature and accordingly, they cannot earn profits. However, these parties can accept voluntary contributions under the Representation of People Act and own ‘immovable property’ which may give them income.

Now, Section 13A gives 100% exemption to political parties on their income from house property, income from other sources, capital gains, and voluntary contributions received from any person.

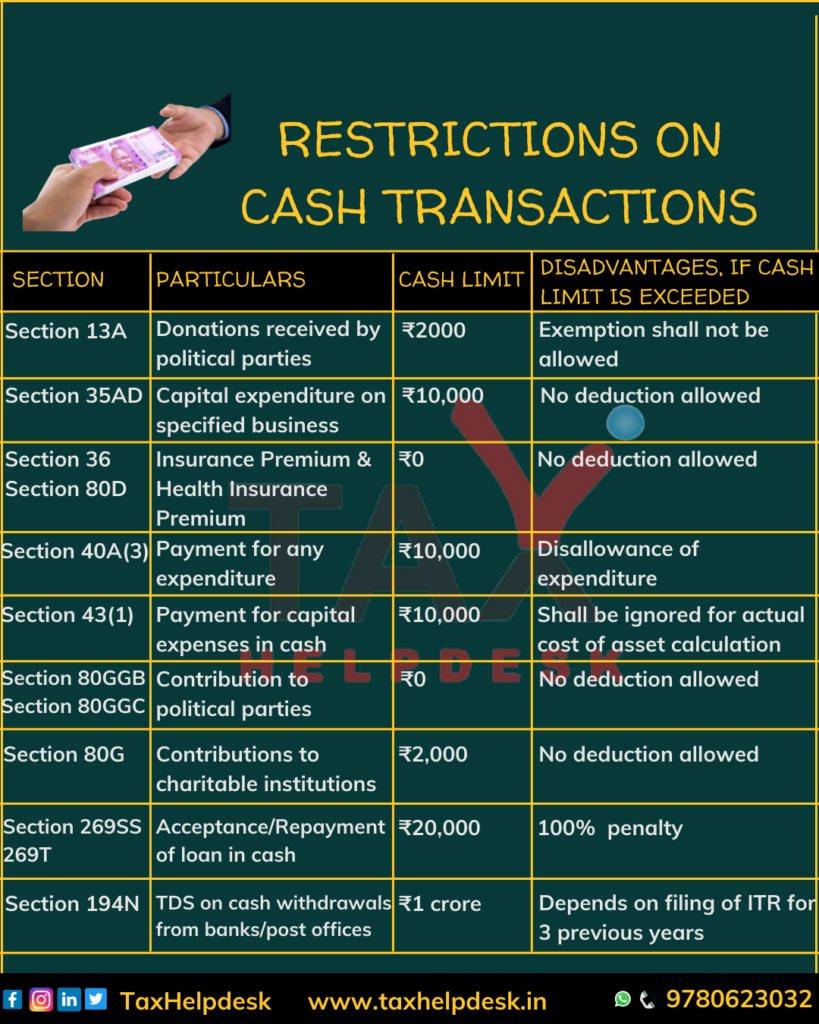

The maximum amount of allowable deduction in cash under this section is Rs. 2000/-.

| Section | Particulars | Cash Limit | Disadvantages if Cash Limit is exceeded |

|---|---|---|---|

| Section 13A | Donations received by political parties | ₹2000 | Exemption shall not be allowed |

Also Read: Deduction Under Section 80C & Its Allied Sections

2. Capital Expenditure On Specified Business (Section 35AD)

Provision of Section 35AD states that the deduction is available towards any capital expenditure, wholly and exclusively, which is for carrying on a specified business.

However, deduction under section 35AD is not available towards expenditure on acquisition of any land or financial instrument or goodwill. Above all, to avail of this deduction, the person has to meet certain conditions.

Further, there is cash payment payment restrictions on payment of more than Rs. 10,000 in a single day.

| Section | Particulars | Cash Limit | Disadvantages if Cash Limit is exceeded |

|---|---|---|---|

| Section 35AD | Capital expenditure on specified business | Rs. 10,000 | No deduction allowed |

Also Read: Income Tax On Agriculture Income Easily Explained By TaxHelpdesk

3. Insurance Premium, Health Insurance Premium (Section 36, 80D)

Section 36 and Section 80D covers deductions on the insurance premium and health insurance premium respectively. These deductions can be claimed only if, the premiums are bought by way of a banking transaction (cheque/demand draft/electronic transfer). Therefore, there is cash payment restrictions on medical insurance deduction.

| Section | Particulars | Cash Limit | Disadvantages if Cash Limit is exceeded |

|---|---|---|---|

|

Section 36 Section 80D |

Deduction on Insurance Premium and Health Insurance Premium | Rs. 0 | No deduction allowed |

Also Read: 10 Ways To Save Your Taxes!

4. Contribution To Political Party (Section 80GGB, 80GGC)

As per Section 80GGB, any Indian company or enterprise that donates to a political party or an electoral trust of India can claim a deduction on the amount of contribution. However, there are cash payment restrictions wrt donation under this section. Accordingly, the person cannot claim deductions under Section 80GGB if the contribution is in cash.

Also Read: A Quick Look At Deductions Under Section 80C To Section 80U

Likewise, Section 80GGC also deals with deductions to political parties. But, the deduction under Section 80GGC can be availed by individuals making contributions to a political party. Furthermore, this section also does not allow to claim deductions, if the contributions are made in form of cash.

| Section | Particulars | Cash Limit | Disadvantages if Cash Limit is exceeded |

|---|---|---|---|

|

Section 80GGB Section 80GGC |

Contribution to Political Party | Rs. 0 | No deduction allowed |

5. Payment For Any Expenditure (Section 40A(3))

There are cash payment restricts on payment for any expenditure under Section 40A(3). However, it allows cash transaction of up to Rs. 10,000 in a single day. To sum it up, if there is any expenditure which is above Rs. 10,000/-, then the payment of the same should be by way of bank transfer/electronic transfer/cheque/demand draft.

| Section | Particulars | Cash Limit | Disadvantages if Cash Limit is exceeded |

|---|---|---|---|

| Section 40A(3) | Payment for any expenditure | Rs. 10,000 | Disallowance of expenditure |

6. Payment of Capital Expenses in Cash

In addition to the above, there are cash payment restrictions on capital expenditures under Section 43. According to this provision, if an assessee makes a payment of an amount equal to or exceeding Rs. 10,000/- in cash to any person in a single day for any expenditure towards the acquisition of any asset, then such sum is not be included in the cost of the asset. Moreover, the assessee will also not be able to claim depreciation on such an amount.

Also Read: Major Exemptions & Deductions Availed By Taxpayers In India

Accordingly, cash transactions of only up to Rs. 10,000 in a single day are allowable as deductions on capital expenditure.

| Section | Particulars | Cash Limit | Disadvantages if Cash Limit is exceeded |

|---|---|---|---|

| Section 43(1) | Payment of capital expenses in cash | Rs. 10,000 | Shall be ignored for calculation of actual cost of asset. |

7. Presumptive Profit (Section 44AD)

Under Section 44AD of the Income Tax Act, small taxpayers with less than 2 crores of turnover do not have to maintain books of accounts. Additionally, their profits are presumed to be 8% of their turnover. For availing benefit under this scheme, profits where income is credited digitally or through the bank will be considered as 6% as against 8% for cash receipts.

Section

Particulars

Cash Limit

Disadvantages if Cash Limit is exceeded

Section 44AD

Presumptive Profit

–

For availing benefit under this scheme, profits where income is credited digitally or through the bank will be considered as 6% as against 8% for cash receipts.

Also Read: Income Tax Audit: Small Taxpayers Or Presumptive Income

8. Contributions To Charitable Institutions (Section 80G)

Certain contributions made to certain relief funds and charitable institutions can be claimed as a deduction under Section 80G. Moreover, donations can be made in cash or through bank transfers. Having stated that, cash contributions above Rs. 2,000/- cannot be used to claim deduction under this section.

| Section | Particulars | Cash Limit | Disadvantages if Cash Limit is exceeded |

|---|---|---|---|

| Section 80G | Contributions to Charitable Institutions | Rs. 2,000 | No deduction allowed |

9. Contributions towards scientific research or rural development (Section 80GGA)

Section 80GGA allows deductions for donations made towards scientific research or rural development. This deduction is allowable to all assessees except those who have an income (or loss) from a business and/or a profession.

Donations can be in the form of a cheque/demand draft/cash. However, there can be no deductions on cash donations over Rs 10,000.

| Section | Particulars | Cash Limit | Disadvantages if Cash Limit is exceeded |

|---|---|---|---|

| Section 80GGA | Contributions towards scientific research or rural development | Rs. 10,000 | No deduction allowed |

Also Read: Taxability Of Pension: All You Need To Know

10. TDS on cash withdrawals from banks/post offices (Section 194N)

If there is no filing of Income Tax Return (ITR) for the last three financial years by an assessee, then cash withdrawal from his/her savings or current bank account will attract TDS if the total amount withdrawn in a financial year exceeds Rs 20 lakh / Rs. 1 crore, as the case may be.

| Aggregate Cash Withdrawal in a Financial Year | TDS Rates, if ITR of last 3 years filed | TDS Rates, if ITR of last 3 years not filed |

|---|---|---|

| Up to ₹20 lacs | NIL | NIL |

| ₹20 lacs – ₹1 crore | NIL | 2% |

| Above ₹1 crore | 2% | 5% |

Note:

Through Union Budget, 2023 the threshold limit for cooperative societies for cash withdrawal is Rs. 3 crores.

Also Read: TDS On Cash Withdrawal (Section 194N) (Expert Guide)

11. Acceptance or Repayment of loan in cash (Section 269SS, 269T)

A person cannot accept loan or deposit or any other specified sum (specified sum here refers to an advance or otherwise, in relation to the transfer of any immovable property) from another person otherwise than by an account payee cheque or account payee bank draft or use of electronic clearing system through a bank account, if –

– Amount of loan or deposit or specified sum is Rs. 20,000 or more, or

– Sum total amount of loan, deposit, and the specified sum is Rs. 20,000 or more.

Therefore, Section 269SS puts a restriction on loans in cash above Rs. 20,000/-

Similar to Section 269SS, Section 269T prohibits any person to repay the loan or deposit or specified sum otherwise than by an account payee cheque or account payee bank draft or by use of an electronic clearing system through a bank account, if –

– Amount of loan or deposit, including interest amount, is Rs. 20,000 or more, or

– The aggregate amount of loans or deposits, including the interest amount, held by such person in his own name, or jointly with any person, is Rs. 20,000 or more.

Therefore, under Section 269T also puts a restriction on loan in cash above Rs. 20,000/-.

| Section | Particulars | Cash Limit | Disadvantages if Cash Limit is exceeded |

|---|---|---|---|

|

Section 269SS Section 269T |

Acceptance/Repayment of loan in cash | Rs. 20,000 | 100% penalty |

Also Read: TDS On Purchase Of Goods Under Section 194Q

12. Cash received for transactions (Section 269ST)

Lastly, Section 269ST prohibits any person to receive an amount of Rs.2 lakh and above in cash:

– In aggregate from a person in a day, or

– A single transaction, or

– In respect of transactions relating to one event or occasion from a person.

Therefore, there is cash payment restrictions under this section above Rs. 2 lacs on the above transactions.

| Section | Particulars | Cash Limit | Disadvantages if Cash Limit is exceeded |

|---|---|---|---|

| Section 269ST | Cash received for transactions | Rs. 2,00,000 | 100% penalty |

If you want to know more about cash payments restrictions or take TaxHelpdesk’s experts consultation, then drop a message below in the comment box or DM us on Whatsapp, Facebook, Instagram, LinkedIn and Twitter. For more updates on tax, financial and legal matters, join our group on WhatsApp and Telegram!

Disclaimer: The views are personal of the author and TaxHelpdesk shall not be held liable for any matter whatsoever!

Pingback: Types of Golden Rules of Accounting | TaxHelpdesk

Pingback: Which Section is applicable – Section 194Q or Section 206C(1H)? | TaxHelpdesk

Pingback: TDS on Cash Withdrawal From Bank in a Financial Year | TaxHelpdesk