TDS on Salary, under Section 192 is to be deducted by employer who pays salary to his employee (resident or non-resident) on his estimated income during every month.

Who has to deduct TDS on Salary under Section 192?

Whenever, there is an employer-employee relationship, TDS under Section 192 is to be deducted. For the various categories of employers, the persons responsible for making payment under the head salaries and for deduction of tax are as below:

| Particulars | Person responsible for deducting TDS on Salary |

|---|---|

| Central/State Government/P.S.U | The designated drawing & disbursing officers |

| Private & Public Companies | The company itself as also the principal officer thereof |

| Firm | The managing partners/partner of the firm |

| HUF | Karta of the HUF |

| Proprietorship Firm | The proprietor of the said concern |

| Trust | Managing trustees thereof |

When is TDS to be deducted under Section 192?

The law essentially requires the deduction of tax when

(a) Payment is made by the employer to the employee.

(b) The payment is in the nature of salary and

(c) The income under the head salaries is above the maximum amount not chargeable to tax.

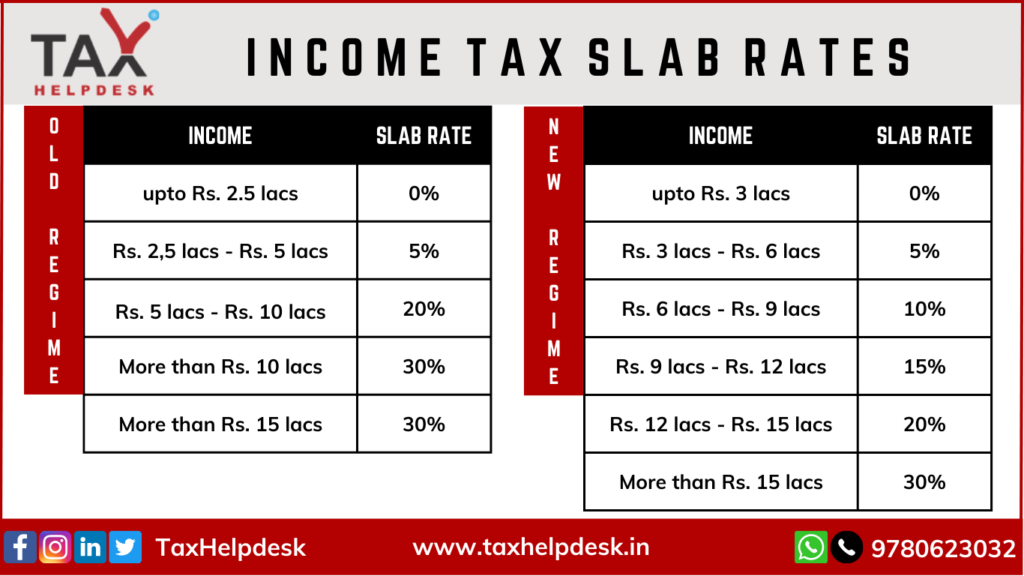

The amount limit from which tax is chargeable is as follows:

| AGE GROUP | OLD TAX REGIME | NEW TAX REGIME |

|---|---|---|

| Individuals below 60 years | ₹2,50,000 | ₹3,00,000 |

| Individuals of age 60 years and above but below 80 years | ₹3,00,000 | ₹3,00,000 |

| Individuals above 80 years | ₹5,00,000 | ₹3,00,000 |

*In case, the taxable income of the employee is less than or equal to Rs. 5 lacs (under the Old Tax Regime) or Rs. 7 lacs (under the New Tax Regime), then no TDS shall be deducted (Rebate under Section 87A)

Rate of TDS on Salary under Section 192

There is no fixed rate of TDS under Section 192. The TDS is calculated on the estimated total income of the employee earned during the relevant financial year at an average tax rate. To compute the rate of TDS, the estimated total tax liability on such estimated income is divided over the period of employment i.e. months.

TDS on salary = Estimated Total Tax Liability

____________________________

Period of Employment

The tax liability is calculated on the basis of Income Tax Slab of the net taxable income of the employee.

Income Tax Slab Chart for the Assessment Year 2024-25:

Calculation of TDS under Section 192

The TDS under Section 192 is calculated on the estimated total tax liability of the person. For this purpose, the employer has to take care of the following points:

a) Income other than salary like rental income is also to be considered by the employer for calculation of TDS on salary if details of such income are submitted by the employee.

b) Interest on home loan (if any) up to Rs. 2,00,000/- will be set off from salary income to arrive at estimated income for TDS calculation, if evidence of the same is given in Form 12BB by the employee.

c) It also happens that many employees make investments to enjoy tax benefits i.e. to reduce their tax liability. But, as the employer does not know about such investments, the TDS amount increases than the actual tax liability. In such cases, the employee can declare information about all his tax-saving investments to the employer using Form 12BB. When an employer sees this, he/she will consider these investments and calculate the TDS amount accordingly.

After the estimated tax liability is ascertained, it is divided by the period of employment to calculate the amount of TDS

ALSO READ | Deduction on interest paid on home loan

Illustration

Illustration 1: The details of income of Sia (opting for old tax regime) for the FY 2022-23 are as follows:

| Particulars | Amount (in Rs.) |

|---|---|

| Gross Salary | 3,60,000 |

| Less: Standard Deduction | (50,000) |

| Income from Rent | 10,000 |

| Gross Total Income | 3,00,000 |

| Chapter VI-A deductions (LIC Policy) | 1,50,000 |

| Taxable Income | Rs. 1,50,000 |

| Tax as per applicable slab rates | 0% |

| Total Tax | 0 |

There shall be no deduction of TDS since the taxable income is below Rs. 2.5 lacs.

Illustration 2:

The TDS calculation of income of Rajeev (opting for old tax regime) are as follows:

| Particulars | Amount (in Rs.) |

|---|---|

| Gross Salary | 12,00,000 |

| Less: Standard Deduction | (50,000) |

| Gross Taxable Income | 11,50,000 |

| Chapter VI-A deductions (LIC Policy) | 1,50,000 |

| Taxable Income | Rs. 10,00,000 |

| Tax as per applicable slab rates | 20% |

| Cess @4% | 4,500 |

| Total Tax | 1,17,000 |

Since, there are 12 months in a financial year, accordingly, the employer will deduct TDS as: Rs. 1,17,000/12 = Rs. 9,750.

Calculation of TDS in Special Cases

There may be cases where the person may have changed his job in a relevant financial year, or is employed at two places or has salary in foreign currency. The calculation of TDS is done as follows:

Change of job during the year

If the employee resigns and joins another employer during the relevant Financial Year, then the details of his previous employment is required to be given in Form 12B to his new employer to deduct TDS properly. Accordingly, the next employer will consider his previous salary and TDS deducted while calculating TDS for the remaining months of the financial year.

Engaged with two or more employers simultaneously

If an employee is engaged with more than one employer simultaneously, then he should provide details about his salary and TDS in Form 12B to any one of his employers. And that one of the employers is required to deduct TDS on aggregate salary.

Salary is payable in foreign currency

First of all salary will be converted into Indian currency.The rate of exchange will be the last day of the month immediately preceding the month in which the salary is due, or is paid in advance or in arrears.

After conversion, calculate TDS as per normal provisions of TDS deduction.

For example, if salary is paid in the month of July in foreign currency, then the rate of exchange shall be taken which prevail on 30th June.

Time limit to deposit TDS under Section 192

The TDS deducted from salary by the employer is required to be deposited to the government within given below timeline to avoid interest:

TDS deducted for April-February: 7th of subsequent month

TDS deducted for March: 30th April

Consequences of Non-Compliances

Levy of Interest : If the employer does not deduct the TDS on salary or deduct the TDS but not deposited to the government then interest @1.5% is required to be paid on such amount.

Disallowance of expenses : Also, the employer is not eligible to claim the deduction of salary expense from Profit and Gains from Business & Profession income, if TDS is not deducted on time.

The amount of disallowed salary expenses shall be

– 30% of Salary payment to Resident.

– 100% of Salary payment to Non-Resident.

Some Important Scenarios

Tips paid to waiters: If tips are paid to the waiter directly or through the employer (which may be paid by the customers), in that case the employer is not responsible to deduct TDS on tip amount, since it does not become part of salary income.

Remuneration paid to directors: Remuneration paid to directors by the company is not covered under section 192. Generally, TDS on remuneration paid to the director shall be deducted under Section 194J, provided there exists no employee employer relationship.

Also Read: GST on Remuneration paid to Directors

Payment made to doctors by the hospital: It is considered as professional fees. Hence, TDS under Section 192 shall not be deducted. But, if it is a contract of service, then TDS under Section 192 shall be deducted.

Non-monetary perquisites: If tax on non-monetary perquisites is borne by the employer, then no TDS is required to be deducted from salary to that extent.

If you want to know more about TDS or want to take TaxHelpdesk’s experts consultation, then drop a message below in the comment box or DM us on Whatsapp, Facebook, Instagram, LinkedIn and Twitter. For more updates on tax, financial and legal matters, join our group on WhatsApp and Telegram!

Disclaimer: The views are personal of the author and TaxHelpdesk shall not be held liable for any matter whatsoever!