Section 80D of the Income Tax Act has double advantages. It provides health insurance as well as tax deductions to the person.

There is a well saying that “better to be safe than sorry”. Our government works on the same policy and to protect the health and promote the welfare being of its citizens, it encourages everyone to invest in Health Insurance Policies. In addition to this, these health insurance policies not only prevent us from unforeseeable situations (like COVID-19) and expenses, but also helps in saving taxes by the way of provisions of the Income Tax Act.

However, there can be cases where the person cannot afford Health Insurance policies, in that case also he can save taxes on medical expenditures. Read this blog to know more!

Provisions in relation to Health Insurance under Section 80D

The provisions in relation to Health Insurance under Section 80D of the Income Tax Act are:

| Section | Particulars |

|---|---|

| Section 80D | Tax deductions on medical expenditures incurred (includes premium paid for Health Insurance for self, parents, children or spouse) |

| Section 80DDB | Tax deductions on expenses incurred towards the treatment of specified diseases |

| Section 80DD | Tax deduction on medical treatment of a dependent who is a person with disability |

Also Read: Know Tax Benefits on Health Insurance and Medical Expenditure

Who Can Claim Deduction?

The individuals and HUFs opting for the old tax regime can only claim a deduction under Section 80D. In other words, the deduction under Section 80D is not available under the New Tax Regime.

Also Read: Income Tax Slabs under the Old & New Tax Regime

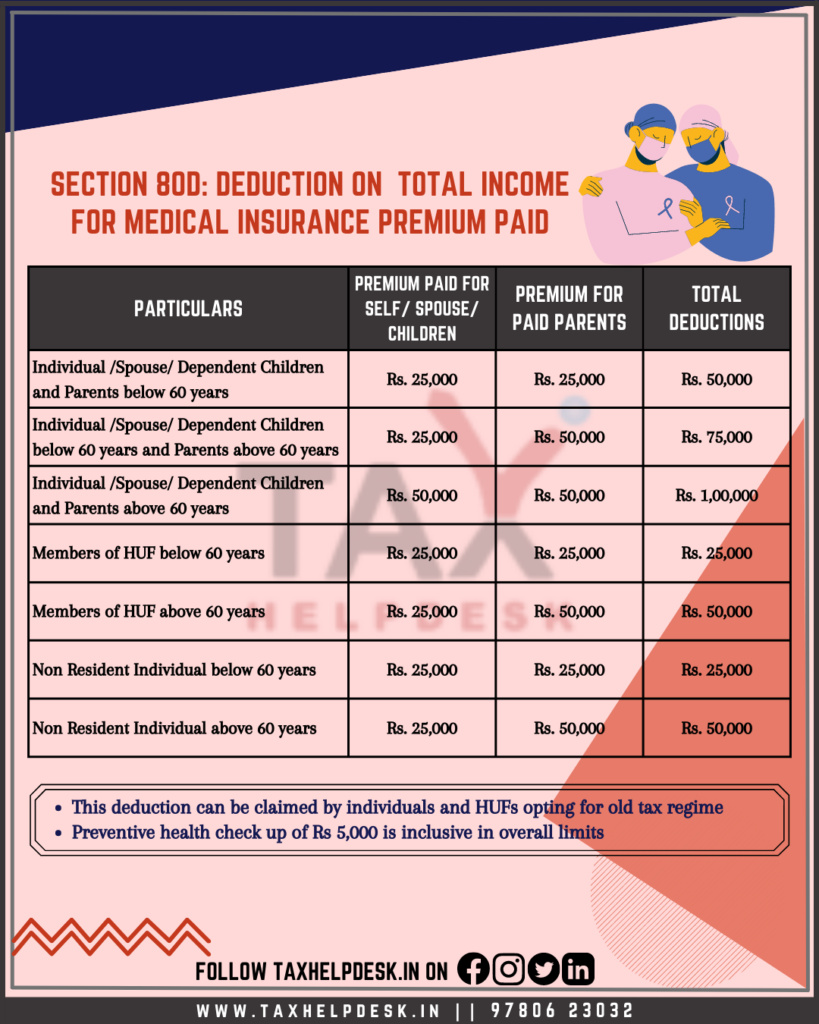

Further, the deduction can be claimed on the person’s total income for medical insurance premium paid and expenses incurred on health and critical illness during a financial year.

80D under income tax Act

Section 80D of the Income Tax Act provides a deduction of up to ₹25,000 in respect of the premium paid towards health insurance of self, spouse and dependent children. This section further, allows a deduction of up to ₹25,000 for the premium paid towards the health insurance policy of the assessee’s parents aged below 60 years and ₹50,000, in case assessee’s parents are aged above 60 years.

Please note that it does not matter whether parents are dependent or not. Further, to claim the deduction on the premium paid towards the health insurance, the payment must be made through the bank.

Also Read: 10 Ways To Save Your Taxes!

Deduction in respect of preventive health check-up

Section 80D also allows a deduction of up to ₹5,000 in respect of payments made towards preventive health check-ups of self, spouse, dependent children or parents made during the previous year. Payment on account of preventive health check-ups may be made in cash.

The deduction of ₹5,000 is inclusive of the overall limit of ₹25,000 or ₹50,000 as the case may be.

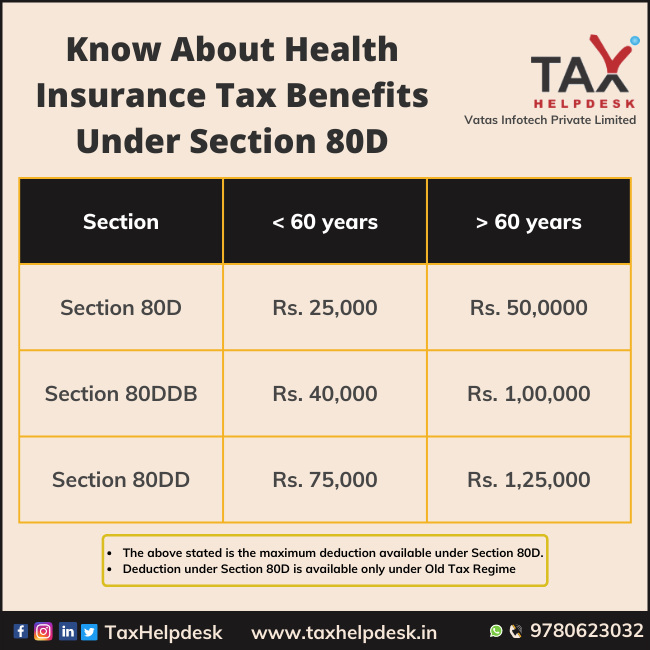

Maximum Limit of Deduction Amount that can be claimed under Section 80D

Specified diseases deduction under Section 80DDB

Section 80DDB allows a tax deduction on expenses which an individual incurs on himself or his dependent on the treatment of specified diseases as stated in the act. The amount that can be claimed as deduction is the sum actually paid or ₹40,000, whichever is lower.

The maximum deduction amount in the case of a senior citizen is ₹1 lakh.

Also Read: New Rules Related To Employee Provident Fund Scheme

The amount of deduction shall be reduced by the amount paid by an insurance company or reimbursed by the employer.

Specified diseases under Section 80DDB are:

| Disease | Certificate to be taken from |

|---|---|

|

Neurological Diseases where the disability level has been certified to be of 40% and above — (a) Dementia (b) Dystonia Musculorum Deformans (c) Motor Neuron Disease (d) Ataxia (e) Chorea (f) Hemiballismus (g) Aphasia (h)Parkinsons Disease |

Neurologist having a Doctorate of Medicine (D.M.) degree in Neurology or any equivalent degree, which is recognised by the Medical Council of India |

| Malignant Cancers | Oncologist having a Doctorate of Medicine (D.M.) degree in Oncology or any equivalent degree which is recognised by the Medical Council of India |

| Full Blown Acquired Immuno-Deficiency Syndrome (AIDS) | any specialist having a post-graduate degree in General or Internal Medicine, or any equivalent degree which is recognised by the Medical Council of India |

| Chronic Renal failure | a Nephrologist having a Doctorate of Medicine(D.M.) degree in Nephrology or a Urologist having a Master of Chirurgiae(M.Ch.) degree in Urology or any equivalent degree, which is recognised by the Medical Council of India |

|

Hematological disorders (i) Hemophilia (ii) Thalassaemia |

a specialist having a Doctorate of Medicine (D.M.) degree in Hematology or any equivalent degree, which is recognised by the Medical Council of India |

Disability deduction under Section 80DD

Sections 80DD of the Income Tax Act covers deduction for the medical treatment (including nursing), training and rehabilitation of a person with a disability. For this section, the expenditure can only be incurred dependent person with a disability. The dependent person can be the spouse, children, parents, brothers and the sisters of the assessee.

Also Read: Can you claim HRA even if you’re staying with your parents?

The amount of deduction that can be availed under Section 80DD is up to Rs. 75,000 for persons having a disability of more than 40% but less than 80%. In cases of severe disability (disability percentage is 80% or more), the maximum deduction that can be availed is up to Rs. 1.25 lacs.

Deduction limits under Section 80DDB and Section 80DD are as follows:

Conclusion

Section 80D of the Income Tax Act covers the following deductions:

| Section | Maximum Deductions for Individual/spouse/dependent children and parents below 60 years | Maximum Deductions for Individual/spouse/dependent children and parents above 60 years |

|---|---|---|

| Section 80D | ₹25,000 | ₹50,000 |

| Section 80DDB | ₹40,000 | ₹1,00,000 |

| Section 80DD | ₹75,000 (disability is more than 40% but less than 80%) | ₹1,25,000 (disability is more than 80%) |

Please not that Section 80DD is not dependent on the age of the person.

If you still have doubts regarding Section 80D, then drop a message below in the comment box or DM us on Whatsapp, Facebook, Instagram, LinkedIn and Twitter. For more updates on tax, financial and legal matters, join our group on WhatsApp and Telegram!

Disclaimer: The views are personal of the author and TaxHelpdesk shall not be held liable for any matter whatsoever!

Pingback: Restriction on Cash Transactions under the Income Tax Act | TaxHelpdesk

Pingback: Section 80U: Deduction in case of disability | TaxHelpdesk

Pingback: Section 80EEA | Deduction on interest paid on home loan | TaxHelpdesk

Pingback: Tax Benefits on Health Insurance and Medical Expenditures | TaxHelpdesk

Pingback: All Important Benefits of Claiming Section 80D ...