In layman’s language, a works contract is a contract of service which may also involve the supply of goods in the execution of the contract. Further, a contract of work may relate to both immovable and immovable property, in a general sense.

Works Contract under GST

Works Contract under GST laws are put under a restriction i.e., they involve works only in relation to “Immovable Property”. In other words, these contracts under GST do not include works in relation to movable property.

Definition of Works Contract

The Works Contract has been defined in Section 2(119) of the CGST Act, 2017 as

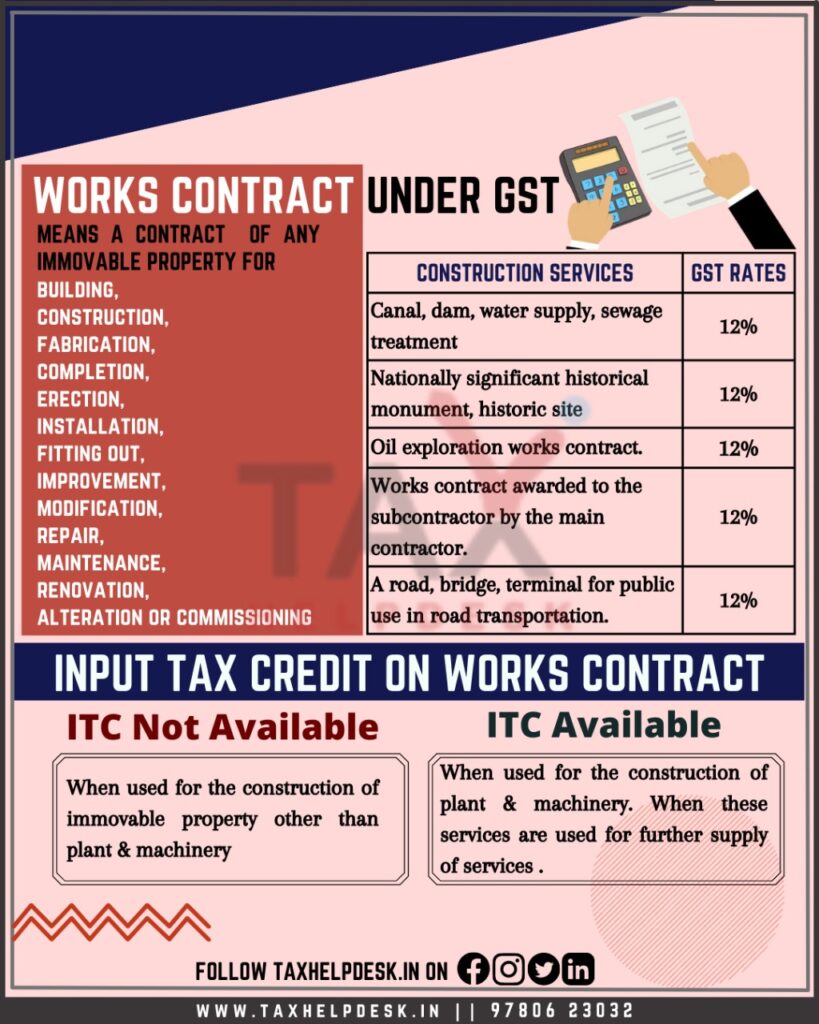

“works contract” means a contract for building, construction, fabrication, completion, erection, installation, fitting out, improvement, modification, repair, maintenance, renovation, alteration or commissioning of any immovable property wherein transfer of property in goods (whether as goods or in some other form) is involved in the execution of such contract.”

Note:

As per CGST Act, works contracts are a supply of services under GST.

Also Read: GST On Land And Building

Input Tax Credit on Works Contract

The Input Tax Credit on work contract under goods and services tax (GST) is available when the services are in use for further supply of services. In addition to this, ITC on such contract is available when services are in use for the construction of plant & machinery.

For instance, a building developer may engage the services of a sub-contractor for a certain portion of the whole work. The sub-contractor will charge goods and services tax (GST) in the tax invoice raised on the main contractor. The main contractor will be able to take ITC on the tax invoice raised by his subcontractor, as his output is works contracts service. However, if the main contractor provides this contract service (other than for plant and machinery) to a company say in the Software business, the ITC of GST paid on the invoice raised by the works contractor will not be available to the Software Company.

In other words, the ITC on these contracts is not available where services

– are not in use for further supply of services

– are in use for construction of immovable property other than plant & machinery.

Place of supply

As stated above, works contract under Goods and services tax in India necessarily involves immovable property. In view of the same the place of supply, where both the supplier and recipient are located in India – the place of supply would be where the immovable property is located. On the contrary, in case the immovable property is located outside India, and the supplier as well as recipient both are located in India, the place of supply would be the location of recipient. Furthermore, in cases where either the supplier or the recipient are located outside India, the place of supply shall be the place where the immovable property is located or intended to be located.

Also Read: Various types of supply under GST

Maintenance of records

As per CGST Rules, 2017, every registered person executing work contracts shall keep separate accounts for work contract showing –

(a) Firstly, the names and addresses of the persons on whose behalf the work contract is under execution;

(b) Secondly, the description, value and quantity (wherever applicable) of goods or services received for such execution;

(c) Thirdly, the description, value and quantity (wherever applicable) of goods or services utilized in the execution;

(d) Fourthly, the details of payment received in respect of each works contract; and

(e) Fifthly, the names and addresses of suppliers from whom he received goods or services.

Also Read: GST E-Way Bill [Ultimate Guide]

GST Rates applicable

| Construction services | GST Rates |

|---|---|

| Canal, dam, water supply, sewage treatment | 12% |

| Nationally significant historical monument, historic site | 12% |

| Oil exploration works contract | 12% |

| Works contract awarded to the subcontractor by the main contractor | 12% |

| A road, bridge, terminal for public use in road transportation | 12% |

If you want to know more about GST or take TaxHelpdesk’s experts for GST consultation, then drop a message below in the comment box or DM us on Whatsapp, Facebook, Instagram, LinkedIn and Twitter. For more updates on tax, financial and legal matters, join our group on WhatsApp and Telegram!

Disclaimer: The views are personal of the author and TaxHelpdesk shall not be held liable for any matter whatsoever!