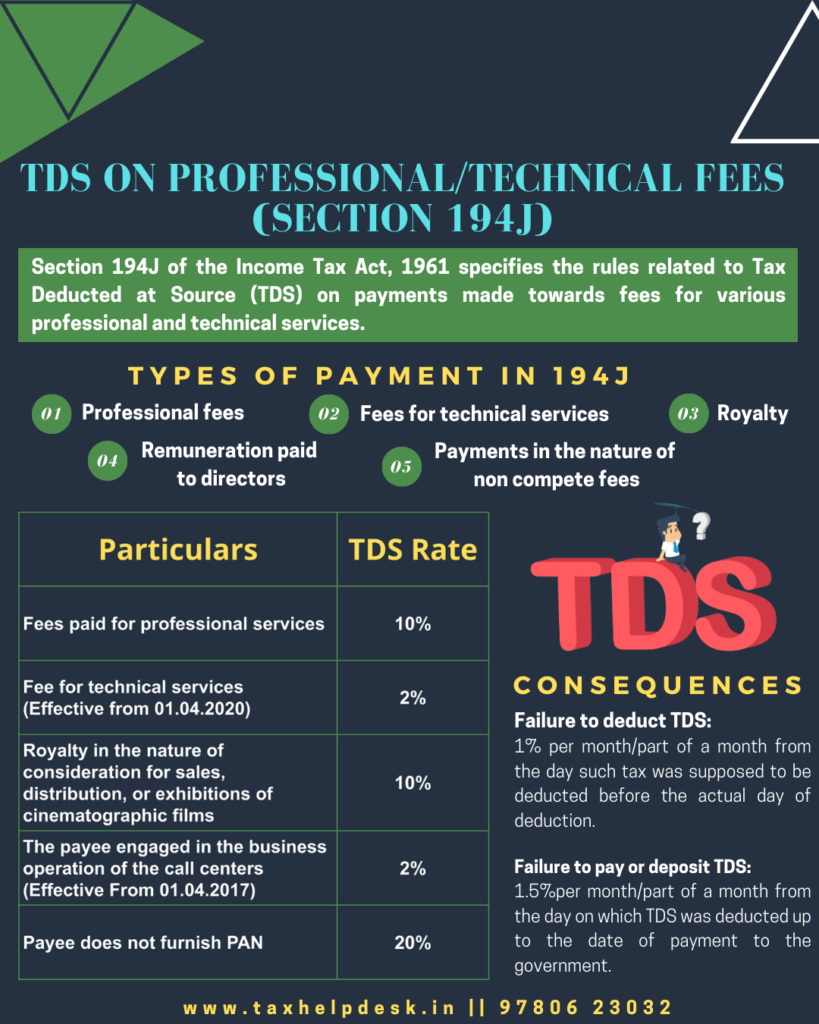

TDS on professional fees or technical services is to be deducted by the person making payment for such services. The same has been provided under Section 194J of the Income Tax Act.

For example, the following fees are covered under Section 194J:

– Professional fees paid to lawyers, doctors, chartered accountants, architects, advertisers, etc

– Technical services fees of rendering of managerial, technical or consultancy services.

Payments Covered Under Section 194J

The payments covered under Section 194J of the Income Tax Act are as follows:

– Professional fees

– Fees for technical services

– Remuneration paid to directors excluding salary (TDS is to be deducted under Section 192)

– Royalty

– Payment in nature of non-compete fees (i.e., fees paid to not carry on any business or profession for a specified time and within certain geographical boundaries) or fees paid to not share any technical knowledge or know-how.

Threshold Limit For TDS Deduction Under Section 194J

TDS on professional fees under Section 194J of the Income Tax Act is to be deducted, in case the payment exceeds the following threshold limits:

| Nature of Payment | Amount |

|---|---|

| Professional fees | Rs. 30,000 |

| Technical services fees | Rs. 30,000 |

| Royalty | Rs. 30,000 |

| Payment in nature of non-compete fees | Rs. 30,000 |

| Remuneration paid to directors | No limit |

Who has to deduct TDS under Section 194J?

TDS under Section 194J is to be deducted by every person, who is making a payment in the nature of professional fees or technical services is liable to deduct tax at source. However, there are certain exceptions, where TDS is not to be deducted:

Individuals or HUFs carrying on business: Where their turnover does not exceed Rs. 1 crore during the previous financial year.

Individuals or HUFs carrying on profession: Where their turnover does not exceed Rs. 50 lakh during the previous financial year.

The services have been taken for personal purposes

In other words, all entities (other than individuals/HUF who are not required to do tax audit in the preceding year) need to deduct tax.

Also Read: TDS On Purchase Of Goods Under Section 194Q

TDS Rates

| Nature of Payment | TDS Rate |

|---|---|

| Professional fees or any payment covered under Section 194J | 10% |

| Technical services fees | 2% (w.e.f., 01.04.2020) |

| Payments made to operators of call centres | 2% (w.e.f., 01.04.2017) |

| If PAN is not furnished | 20% |

When is TDS to be deducted?

The tax should be deducted at the time of-

– Passing such entry in the accounts or

– Making the actual payment of the expense,

whichever earlier.

Illustration

Illustration 1: Piyush took TDS and income tax consultation services of lawyer for handling his company’s case. The lawyer charged him Rs. 20,000 for the same.

– No TDS under Section 194J is to be deducted. Reason being that despite the services were taken from the professional, the amount charged is less than Rs. 30,000/-.

Illustration 2:

Ashneer has availed professional service from Aman in F.Y. 2021-22. First payment was made in April month of Rs. 75000 and second payment in December month of Rs. 25000.

Let us check the TDS liability for both the payments for the F.Y. 2021-22 in three scenarios:

1. Ashneer is not liable for audit under Section

2. Ashneer is liable for audit under Section 44AB and services were taken for personal purpose.

3. Tax audit under Section 44AB is applicable to Ashneer in F.Y. 2021-22 and services were taken for professional service for business purpose.

Case 1

Since Ashneer is not liable for Tax Audit under Section 44AB, he is not liable to deduct tax while making payment to Aman.

Case 2

Though Ashneer has taken professional service but that was for personal purpose. Hence, no TDS is required to be deducted while making payments for such services.

Case 3

If Tax Audit is applicable to Ashneer and he avails the professional tax registration services for business purpose, then TDS @10% must be deducted at Rs. 75,000 while making payment or credit in the accounts, whichever is earlier. This is because the transaction has exceeded the threshold limit of Rs. 30,000.

Similarly, since the transaction amount has exceeded the threshold limit in the financial year, TDS should be deducted for all the payments made to Ashneer. Hence, tax shall be deducted at source on second payment of Rs. 25,000 also.

Also Read: Pay Double TDS On Non-Filing Of ITR

Time for payment

| Particulars | Time limit to deposit TDS |

|---|---|

| If amount is paid or credited in the month of March | On or before 30th April |

| If amount is paid or credited in the month other than March | Within 7 days from the end of the month is which deduction is made |

Due dates for TDS return filing

| Quarter | Quarter Period | Last date of filing |

|---|---|---|

| Q1 | 1st April – 30th June | 31st July |

| Q2 | 1st July – 30th September | 31st October |

| Q3 | 1st October – 31st December | 31st January |

| Q4 | 1st January – 31st March | 31st May |

Penalties Associated with Non or Late Deduction of TDS

Levy of Interest : If the specified person does not TDS return filling or deducting TDS but does not deposit it to the government on time, then interest @1.5% is required to be paid on such amount.

Disallowance of expenses : Further, the person is not eligible to claim the deduction of expenses from Profits and Gains from Business & Profession income, if TDS is not deducted on time. The amount of disallowed expenses shall be 30% of payment

However, if TDS is deposited in subsequent years, then expense will be allowed in the year of payment of TDS.

Also Read: Rate Chart Of TDS For FY 2021-22 AY 2022-23

If you want to know more about TDS or take TaxHelpdesk’s experts consultation, then drop a message below in the comment box or DM us on Whatsapp, Facebook, Instagram, LinkedIn and Twitter. For more updates on tax, financial and legal matters, join our group on WhatsApp and Telegram!

Disclaimer: The views are personal of the author and TaxHelpdesk shall not be held liable for any matter whatsoever!