The penalty for late filing of ITR is payable wherein the person file its income tax return after the due date. The quantum of penalty however, depends upon the total income of the person.

Applicability of penalty for late filing of ITR

The penalty for late fees is applicable when the person who has to mandatorily file the Income Tax Return does not file it within the due date. Consequently, the cases where the person has to mandatorily file ITR are as follows:

– The total income exceeds the basic exemption limit

If the total income of the person exceeds the basic exemption limit under the new tax or old tax regime, he or she must file ITR. Accordingly, the basic exemption limit under both the tax regimes is as follows:

| AGE GROUP | OLD TAX REGIME | NEW TAX REGIME |

|---|---|---|

| Individuals below 60 years | ₹2,50,000 | ₹3,00,000 |

| Individuals of age 60 years and above but below 80 years | ₹3,00,000 | ₹3,00,000 |

| Individuals above 80 years | ₹5,00,000 | ₹3,00,000 |

Note:

For the FY 2022-23, the threshold limit under the new tax regime is Rs. 2,50,000. On the other had, through Union Budget, 2023 there is an increase in this limit and accordingly, it now stands at Rs. 3,00,000.

Also Read: Income Tax Slabs under the Old & New Tax Regimes

Please note that the total income is after claiming all the exemptions, allowances, and deductions.

– If the business turnover is more than Rs. 60 lacs

If a person’s total sales, turnover, or gross receipts for the preceding year exceed Rs 60 lakh, then he or she must file a tax return.

- The professional gross receipts exceed Rs. 10 lacs

In the case of a person whose total gross receipts from his or her profession exceed Rs 10 lakh in the preceding year, then he has to file ITR.

– Total amount of TDS/TCS is Rs. 25,000 or more

If the total amount of TDS and TCS in his case during the previous year was Rs 25,000 or more, then an individual (under 60 years of age) has to file his return. On the other hand, in the case of a resident senior person, whose age is 60 years or more at any point during the preceding year, the threshold limit is Rs 50,000.

Also Read: Difference between TDS & TCS easily explained

– Deposits in the savings bank account or current account

In case, the individual makes deposits of Rs. 50 lacs or more in one or more savings bank accounts during the previous year, then he must file ITR. Alternatively or additionally, if the individual makes deposits of Rs. 1 crore or more in one or more current accounts during the previous year, then also he must file ITR.

– Assets outside India

An individual must file a tax return if he/she:

– Firstly, has (as a beneficiary or otherwise) any asset (including any financial interest in any company) located outside of India

– Secondly, has signing authority in any account located outside India

– Lastly, is a beneficiary of any asset located outside of India (including any financial interest in any organization).

Note:

The above clauses apply to residents as well as non-residents.

- If you spend Rs 2 lakh on international travel

Individual spending more than Rs 2 lakh on travel to a foreign nation for himself or anybody else in the financial year also has to file a return.

Also Read: Best Ways to Save Taxes in 2022

– Lastly, if your annual electricity bill is Rs 1 lakh

In addition to the above, if a person has more than Rs 1 lakh bill on power consumption in the preceding year, then he or she must file a return.

Who has to pay penalty on late filing of ITR?

The penalty for late ITR filing in India is applicable to following persons:

– Individuals

– HUFs

– Company

– Partnership Firms as well as LLPs

– Association of Persons as well as Body of individuals

– Trusts, etc

Due dates for filing of ITR

The due dates for filing of ITR are as follows:

| Category of Taxpayer | Due Date for Tax Filing- FY 2022-23 *(unless extended) |

|---|---|

| Individual / HUF/ AOP/ BOI (books of accounts not required to be audited) | 31st July 2023 |

| Businesses (Requiring Audit) | 31st October 2023 |

| Businesses requiring transfer pricing reports (in case of international/specified domestic transactions) | 30th November 2023 |

| Revised return | 31 December 2023 |

| Belated/late return | 31 December 2023 |

*The due dates may be subject to change

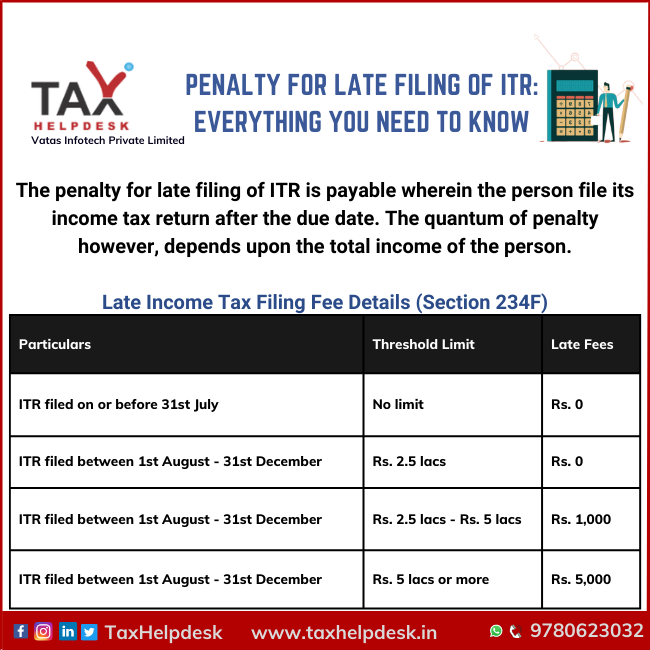

How much penalty is applicable for late filing of ITR?

The penalty for late filing of ITR is applicable as per Section 234F, which is as follows:

| Particulars | Threshold Limit | Late Fees |

|---|---|---|

| ITR filed on or before 31st July | No limit | Rs. 0 |

| ITR filed between 31st July – 31st December | Rs. 2.5 lacs | Rs. 0 |

| ITR filed between 31st July – 31st December | Rs. 2.5 lacs – Rs. 5 lacs | Rs. 1,000 |

| ITR filed between 31st July – 31st December | Rs. 5 lacs or more | Rs. 5,000 |

Illustration

| Total Income | Return Filing Date | Amount of Fees | u/s 234F Reason |

|---|---|---|---|

| 2,30,000 | Not filed | NA | Income is below the exemption limit |

| 3,50,000 | 31/03/2022 | NA | ITR filed before the due date |

| 4,30,000 | Not filed | 1000 | Income is below Rs. 5 lacs |

| 8,50,000 | 30/11/2022 | 5000 | Income is above Rs. 5 lacs |

FAQs

Taxpayers who do not file their ITR by the due date can face fines and prosecution for a period of 3 months t 2 years by the Income Tax Department. Therefore, you can be sent to jail if you do not file ITR within the due date.

In addition to the income tax penalty, the IT Department can charge interest 1% per month till the date of payment of tax.

The payment of late fees under Section 234F is through Challan No. 280, available on NSDL’s website. Consequently, the person can choose

type of payment as Self-assessment (300) and thereby, fill 234 F amount in column “Others”.

Click here to join our Telegram Channel today!