Updated Return & Revised Return are major parts when it comes to filing of Income Tax Return. And, the concept of updated return was introduced recently through the Union Budget, 2022.

What is Updated Return?

Updated Return, as the name suggests is a return that allows the taxpayers to correct any omissions or errors in their previous income tax return or enables them to file a new ITR if they have not filed it previously. However, the period for filing of updated ITR is 24 months from the end of the relevant assessment year. Accordingly, the earliest year for filing this type of return is the Financial Year 2021-2022.

To sum it up, the updated return can be used to

– File ITR not filed earlier

– Make corrections in disclosure in Income Tax Return

– Reduce Income Tax Credit

– Fix or change the head of income

– Reduce the carry forward loss

– Reduce unabsorbed depreciation

– Correct the wrong rate of tax

– Others

What is Revised Return?

A Revised Return, on the other hand, is a return that allows the taxpayers to only correct any omissions or errors made at the time of filing their original return. Accordingly, a revised return is a revisiting of the previously filed return and putting the correct information. Further, the period for filing of revised return is three months prior to the end of the relevant assessment year or before the completion of the assessment year, whichever is earlier. Therefore, the last date for filing of revised ITR for FY 2023-24 is December 31, 2024.

Also Read: Income Tax Return For Small Taxpayers Or Having Presumptive Income

Key differences between the Updated & Revised Return

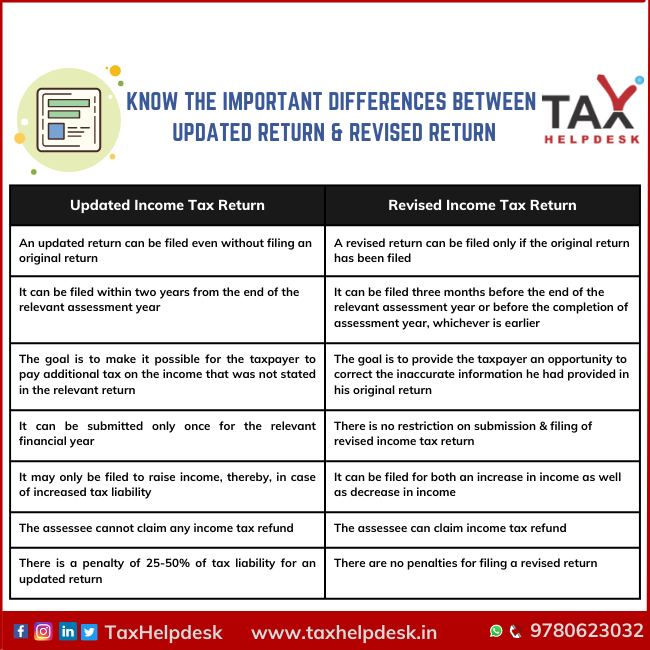

- Filing of original return:

In the case of an updated return, ITR can be filed even without filing an original return. Whereas, for filing a revised return, the filing of the original return is mandatory. - Period:

An updated return can be filed within two years from the end of the relevant assessment year. However, the original return is to be filed within three months prior to the end of the relevant assessment year or before the completion of the assessment year, whichever is earlier. - Goal:

The goal of an updated Income Tax Return is to make it possible for taxpayers to pay additional taxes on the income that was not stated in the relevant return. On the other hand, the goal of a revised return is to provide the taxpayer an opportunity to correct the inaccurate information he had provided in his original return. - Submission:

The updated return can be submitted only once for the relevant financial year. Whereas, in the case of the revised return, there is no restriction on the frequency of submission. Accordingly, revised returns can be filed multiple times within the stipulated time period. - Income Tax Liability:

An updated return can only be filed to raise income, thereby, in case of increased tax liability. However, the revised return can be filed for both an increase in income as well as a decrease in income. - Refund:

In case of an updated return, the assessee cannot claim any income tax refund. However, he can claim the ITR refund by the filing of revised return. - Penalty:

There is a penalty of 25-50% of tax liability for an updated return. On the other hand, there are no penalties for filing a revised return.

FAQs

Every assessee can file an updated return, if his case falls in either of the following four scenarios:

– If he has filed original return under Section 139(1)

– Belated return has been filed under Section 139(4)

– If the assessee has filed original or belated return and thereafter, has filed a revised return under Section 139(5)

– Lastly, if the assessee has not filed the return at all under any of the above sections.

Revised return can be filed by every assessee who has filed an original return or a belated return. While filing of revised return, the assessee has to mention the acknowledgement number and date of the previous filed return in the revised return form.

Updated Return can be filed by using the ITR-U form. Whereas, the revised return can be filed by opting for the option “Revised under Section 139(5)” in the “Return filed under” column.