The investments mentioned under Section 80C are the most popular and preferred way of saving taxes opted by the taxpayers. This is so because the deductions under Section 80C and its allied sections allow a maximum deduction of up to Rs. 1.5 lacs every year from the taxpayer’s total income and an additional deduction amount of Rs. 50,000 can be claimed under Section 80CCD(1b).

Note:

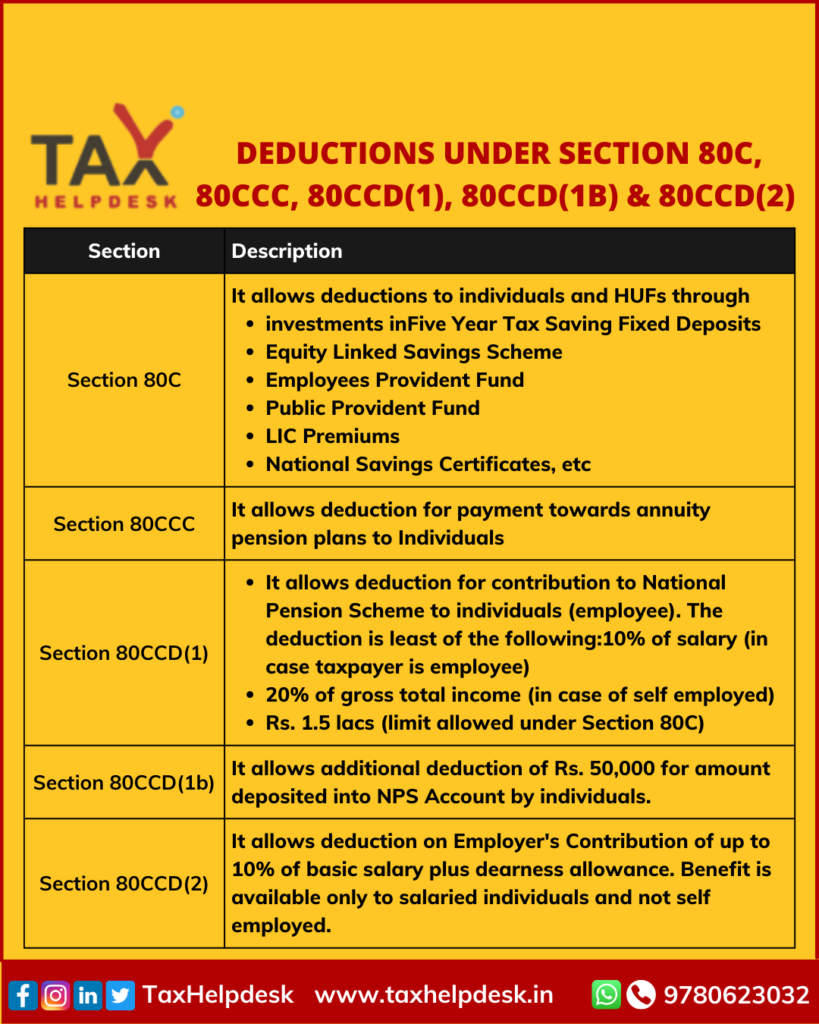

The allied sections of Section 80C are Section 80CCC, Section 80CCD(1), Section 80CCD(1b) and Section 80CCD(1b)

Who can avail the deductions under Section 80C?

The deduction under Section 80C can be claimed only by Individuals (Resident or Non-Resident) and HUFs. Accordingly, the companies, partnership firms, corporate bodies, and others are not eligible to avail the deduction under these sections.

Also Read: A Quick Look at Deductions under Section 80C to 80U

Bifurcation Of Deductions And Its Allied Sections

Options To Save Taxes Through Deductions Under Section 80C

1.Five Year Tax Saving Fixed Deposits

The 5-Year Tax Saving Fixed Deposits, as the number suggests have a lock-in period of 5 years to be eligible for claiming the deductions. These fixed deposits can be opened either at banks or post offices. The interest amount on such deposits is fully taxable. Further, it is to be noted that not all 5-year tenure FDs are tax-saving FDs. This is because the 5-Year Tax Saving FDs are the separate types of FDs offered by the banks or post offices. There are guaranteed returns on these FDs, and the risk profile is low.

2.Equity Linked Savings Scheme (ELSS)

ELSS is a type of mutual fund scheme wherein, 65% of the portfolio is invested in equity and equity-linked securities such as listed shares. And, this scheme has a lock-in period of 3 years, the returns are dependent on the market and the risk profile is high. Further, the Long Term Capital Gains on ELSS are tax-exempted up to Rs. 1 lac, and the dividend earned is tax-free in the hands of the investor.

Also Read: 10 Ways To Save Your Taxes!

3. Employees Provident Fund (EPF)

Employees Provident Fund Scheme is a welfare scheme for the better future of the employees in an organisation. Under this scheme, both employer and employee have to contribute to the EPF. To claim this deduction, the employee cannot withdraw the amount in EPF until he’s 5 years of services are completed. Further, the interest earned on EPF contribution by the employee is taxable and the risk factor of returns is low.

Some More Options to Claim Deductions Under Section 80C

4.Public Provident Fund (PPF)

Public Provident Fund or PPF is a savings cum tax savings investment scheme, the corpus of which can be used at the time of retirement. The interest earned and the returns on this PPF scheme are not taxable and the PPF account can be opened either at a nationalised bank or post office. The lock-in period of PPF is 15 years and it can be further extended in blocks of 5 years.

5.Life Insurance Corporation Premium (LIC Premium)

The LIC premium can be bought either for the individual himself or his family members. In addition to this, the amount that can be claimed as a deduction on Life Insurance Premiums is as follows:

| Policy Taken on | Deduction Available |

|---|---|

| Before 1st April, 2003 | Full premium amount |

| Between 1st April, 2003 and 31st March, 2012 | 20% of sum assured |

| On or after 1st April, 2012 | 10% of sum assured |

The lock-in period for Life Insurance premiums is 5 years and the returns on life insurance policies. In addition to it is where the insurance cover is at least 10 times the annual premium, are exempted from tax under Section 10(10D) of the Income Tax Act.

6. National Savings Certificate (NSC)

NSC is a fixed investment plan scheme that can be opened at any post office in India. The current rate of interest on NSC is 6.8% p.a. The lock-in period is 5 years. The returns on this investment are ensured, as it is backed by the government and the risk profile is low. One can claim deductions by investing in NSC. However, the interest on the amount invested in NSC is taxable.

Also Read: Do I Need To File Income Tax Returns?

Other Important Options to Save Taxes Under Section 80C

7. Principal Amount Payment towards Home Loan

The home buyers can claim a deduction of up to Rs. 1.5 lacs under Section 80C through buying of house property. The deduction on a home loan is available where the buyer purchased the property by way of a home loan. Further, under this scheme, per se there is no lock-in period to avail of the deduction, however, the property should not be sold within 5 years of its possession.

Also Read: Tax Benefits on Home Loan: Know Everything at TaxHelpdesk

8. Senior Citizens Savings Scheme (SCSS)

The Senior Citizens Savings Scheme, as the name suggests is a scheme meant for senior citizens aged above 60 years or individuals aged between 55-60 years, who have opted for the Voluntary Retirement Scheme or retired defence personnel of age above 50 years and below 60 years. Having said this, the SCSS account can also be opened either at post offices or any authorized bank. The current rate of interest for investing in SCSS is 7.4% p.a. with a lock-in period of 5 years and the risk profile is low. The Interest on SCSS is taxable as per the tax slab applicable to the person. In case, the interest amount earned is more than Rs. 50,000 for a financial year, Tax Deducted at Source (TDS) applies to the interest earned.

Also Read: Deductions on interests earned by Senior Citizens

Even More Options To Save Taxes Under Section 80C

9. Sukanya Sammridhi Yojana

The Sukanya Samriddhi Account is designed to provide a bright future for the girl child. The account can be opened in the name of the girl child till she attains the age of 10 years. It offers a high interest rate of 7.6% – 8% along with the deductions under Section 80C. Having said that, the account shall mature on completion of 21 years from the date of opening of the account. However, where the marriage of the account holder takes place before the completion of such a period of 21 years, the minimum lock-in period of this scheme is 18 years, the returns are tax-free and the risk is low.

10. Tax-Free Bonds

Tax-free bonds are issued by the government to raise funds for a specific purpose. These bonds are offered by various Government Public Sector Companies like NHAI, NTPC, REC, REl, HUDCO and others. These tax-free bonds offer a fixed rate of interest and the risk profile is low. And, these bonds have a lock-in period of 10 to 20 years and can be bought through NSE or BSE.

Taxability of various instruments under Section 80C

Conclusion:

The deduction of only up to Rs. 1.5 lacs (collectively) is allowed under Section 80C of the Income Tax Act. However, the taxpayer cannot claim the whole amount invested or spent as deduction under this section.

Also Read: Can I Claim HRA Even If I’m Staying With My Parents?

Note: The above list is only inclusive and not exhaustive.

The analysis as well as rate of returns for investments under Section 80C are as follows:

| Investment options | Interest | Lock-in period for | Risk involved |

|---|---|---|---|

| National Savings Certificate | 6.8% | 5 years | Low |

| Sukanya Samriddhi Yojana | 8% | Till girl child reaches 21 years of age (partial withdrawal is allowed when she reaches 18 years) | Low |

| Tax saving Fixed Deposits | 5.5% – 7.5% | 5 years | Low |

| Public Provident Fund | 7.1% | 15 years | Low |

| Equity Linked Savings Scheme funds | 12% – 15% | 3 years | High |

| National Pension Scheme | 8% – 10% | Till 60 years of age | High |

| Unit Linked Investment Plan | 8% – 10% | 5 years | Medium |

| Senior citizen savings scheme | 8.20% | 5years (can be extended for other 3 years) | Low |

*The above table is subject to change periodically as per the government’s announcements.

If you still have doubts regarding Section 80C, then drop a message below in the comment box or DM us on Whatsapp, Facebook, Instagram, LinkedIn and Twitter. For more updates on tax, financial and legal matters, join our group on WhatsApp and Telegram!

Disclaimer: The views are personal of the author and TaxHelpdesk shall not be held liable for any matter whatsoever!

Pingback: Restriction on Cash Transactions under the Income Tax Act | TaxHelpdesk

Pingback: Section 80U: Deduction in case of disability | TaxHelpdesk

Pingback: Deductions on Interest on Deposits in Savings Account: Section 80TTA | TaxHelpdesk

Pingback: How to claim deductions if you do not get HRA? | Section 80GG | TaxHelpdesk

Pingback: Deductions on interest earned by Senior Citizens | Section 80TTB | TaxHelpdesk

Pingback: Section 80G: Deductions on Donations | TaxHelpdesk

Pingback: Section 80EEA | Deduction on interest paid on home loan | TaxHelpdesk

Pingback: 10 Ways to Save Your Taxes! | TaxHelpdesk

Pingback: which Tax Regime Suits you: Old v. New? | TaxHelpdesk

Pingback: Know about public provident fund | TaxHelpdesk

Pingback: Decoding Section 87A: Rebate Provision under Income Tax Act | TaxHelpdesk

Pingback: Income Tax on Income of Minor Child | TaxHelpdesk

Pingback: Tax Saving Fixed Deposit : 12 Things you should know | TaxHelpdesk

Pingback: Know tax benefits of purchasing property through Home Loan | TaxHelpdesk