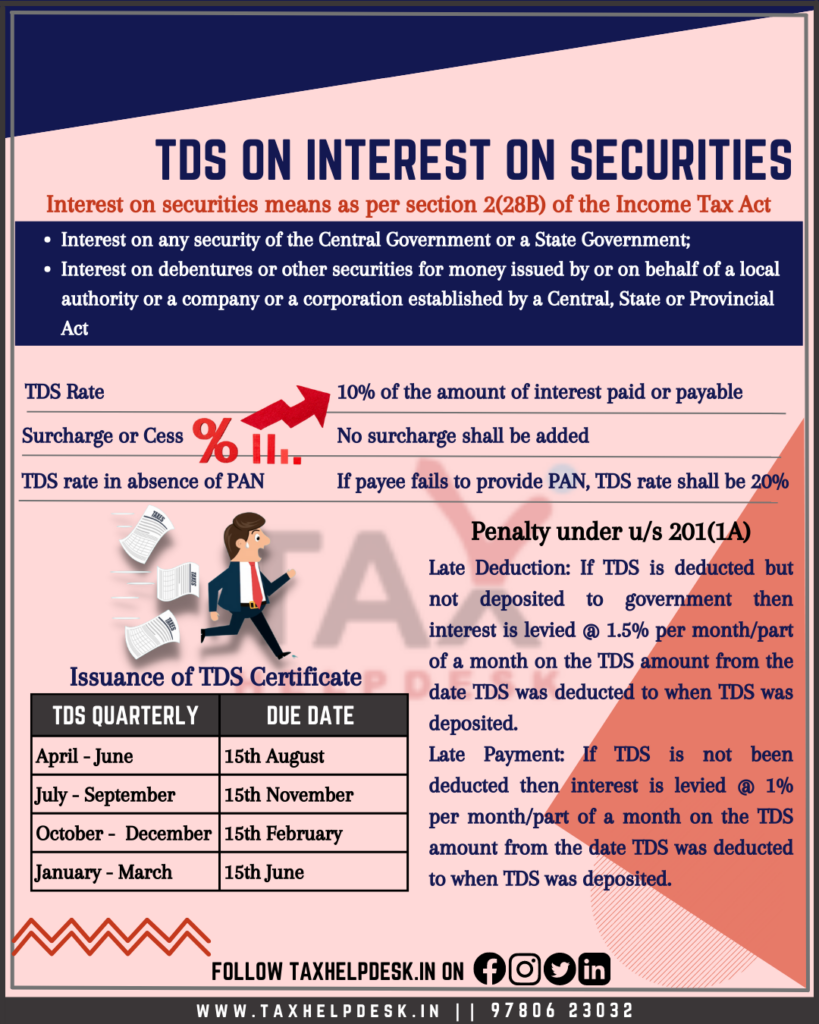

The provisions relating to TDS on interest on securities are covered under Section 193. If a person sends a resident any income in the form of interest on securities, he or she must deduct tax under section 193.

Applicability of TDS on Interest on Securities

As per Section 193, provisions of TDS on interest on securities apply only to resident individuals. As a result, at the time of paying interest on securities to a non-resident, the application of section 193 does not apply. Further, Section 195 deals with TDS on Non Residents.

In this blog, we will discuss the concept of Section 193 of the tax deduction.

Also Read: Understand TDS Deduction: If Person Is Resident In India

Who deducts TDS on Interest on Securities?

Every person who is responsible to pay interest on securities to a resident, is liable to deduct tax at source under section 193.

Cases where TDS on Interest on Securities is not applicable

Some cases where there is no deduction of TDS on interest are as follows:

– If the payee provides a self-declaration in Form 15G/15H to the payer to the effect that his income falls below the exemption limit;

– When the payee has obtained a certificate from the Assessing Officer for no deduction or lower deduction of tax;

– Payable interest to LIC/ other insurers on securities owned by them or in which they have full beneficial interest.

– Interest payable on security (which is in demat form) issued by a company listed on stock exchange in India

– 7 year National Savings Certificate (IV issue) interest.

– National Development Bonds interest

– 4% National Defence Loan, 1968 or National Defence Loan, 1972 interest held by an Individual.

– 4% National Defence Bonds, 1972 interest held by a resident Individual.

– GIC (General Insurance Corporation) interest on the securities owned by it or in which it has a full beneficial interest.

– 6 % Gold Bonds, 1977 or 7% Gold Bonds, 1980 interest held by a resident

– Interest on Security of the Central Government or a State Government

– Interest to any other insurer on the securities owned by it or in which it has a full beneficial interest.

Also Read: Section 192: TDS on Salary

TDS on interest on debentures and bonds

For interest on debentures issued by a company, there is no deduction of TDS under Section 193 if payment is within the threshold limit as follows:

| Payer | Payee | Threshold Limit |

|---|---|---|

| Widely held company | Resident Individual or HUF | Interest does not exceed Rs. 5,000 and interest is paid by an account payee cheque. |

Further, for interest on 8% Savings (Taxable) Bonds 2003 and 7.75% Savings (Taxable) Bonds 2018, TDS on interest on securities under Section 193 is not deducted if payment is within the threshold limit of Rs. 10,000.

Illustration

For example, Mr. X has invested some amount in ABC Limited and the company has paid him an interest of Rs. 4,50,000 after deducting tax at source @10%. In this case, his tax liability and tax refund, if any for AY 2020-21 will be computed as follows:

| Particulars | Amount |

|---|---|

| Income from Other sources – Gross Interest (4,50,000/90%) | Rs. 5,00,000 |

| Total income | Rs. 5,00,000 |

| Tax on Rs. 5,00,000 | Rs. 12,500 |

| Less: Rebate under Section 87A | Rs. 12,500 |

| Tax liability | Nil |

| Less: TDS | 50,000 |

| Refund | 50,000 |

Thus, Mr. X can claim full refund of TDS at the time of filing his ITR.

Also Read: Know Types Of TDS Certificates

Rate & time of TDS under Section 193

The rate of tax under Section 193 is 10%. Consequently, the time of deduction is earlier of

– the credit of income to the account of the payee (receiver) or

– actual payment (in cash, cheque, draft or other modes).

However, if the payee does not furnish his Permanent Account Number (PAN), then the payer has to deduct tax at the higher of the following:

– Rate specified in the relevant provision of the Income-tax Act.

– The rate or rates in force, i.e., the rate prescribed in the Finance Act.

– At the rate of 20%.

Due date of filing TDS returns

| Quarter | Quarter Period | Last date of filing |

|---|---|---|

| Q1 | 1st April – 30th June | 31st July |

| Q2 | 1st July – 30th September | 31st October |

| Q3 | 1st October – 31st December | 31st January |

| Q4 | 1st January – 31st March | 31st May |

Penalty for late payment and late filing

Late Deduction: In case, TDS has been deducted but not deposited to the government, then in that case interest will be levied @1.5%per month or part of a month on the amount of TDS from the date in which TDS was deducted to the date in which TDS was deposited.

Late Payment: In case, TDS has not been deducted then in that case interest will be levied @1%per month or part of a month on the amount of TDS from the date in which TDS was deducted to the date in which TDS was deposited.

Section 234E: Penalty under this section is Rs. 200 per day till the failure continues by the deductor. However, the amount of penalty cannot be more than the amount of TDS return filing needs to be filed.

If you want to know more about TDS or take TaxHelpdesk’s experts consultation, then drop a message below in the comment box or DM us on Whatsapp, Facebook, Instagram, LinkedIn and Twitter. For more updates on tax, financial and legal matters, join our group on WhatsApp and Telegram!

Disclaimer: The views are personal of the author and TaxHelpdesk shall not be held liable for any matter whatsoever!