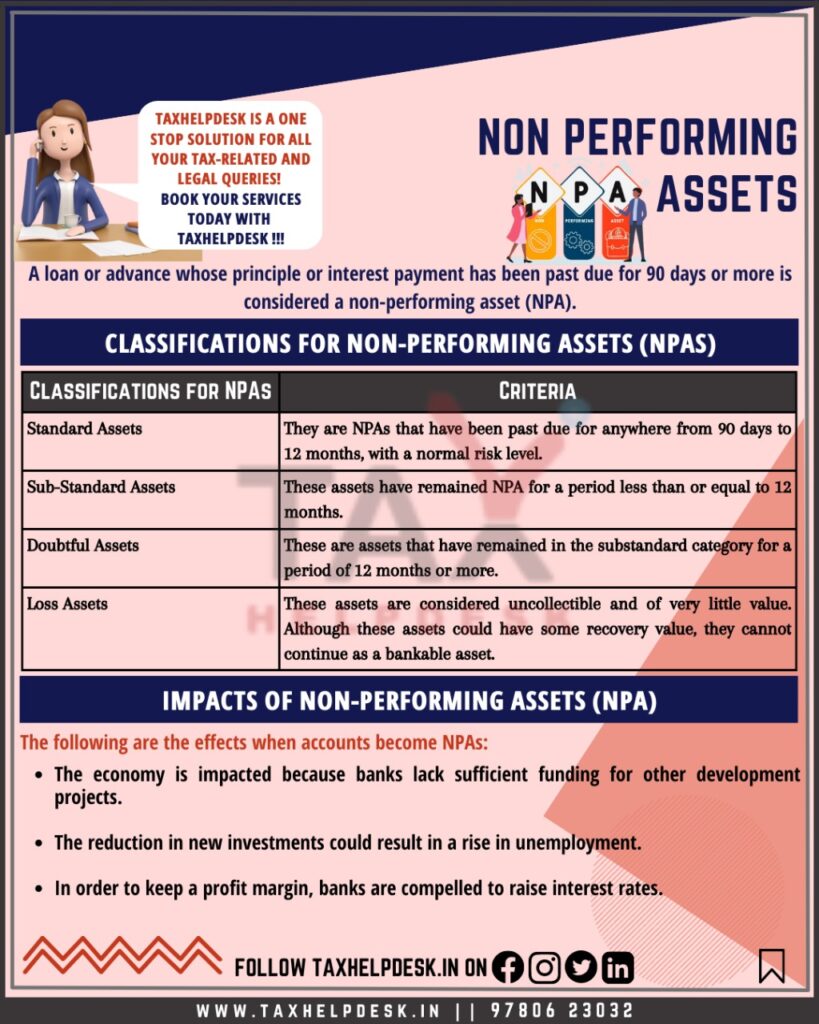

Non Performing Assets or NPA are those assets whose loan or advance against the principal or interest payment is overdue for more than 90 days.

How do You Identify Non Performing Assets?

One can identify the non performing assets through the following parameters:

- An auditor can look into the functioning of a bank with the verification of the Concurrent Audit report. This will give them insight into the irregularities of the loans.

- Screening accounts is an effective way to verify credits from legitimate accounts at the end of each month. It classifies the advances of a bank that can prevent a cash credit account from becoming an NPA.

- Accounts have different coding. For example, an agricultural account will not become an NPA after 90 days but waits for income for two crop seasons which can take up to 12 months.

- If the primary security didn’t submit stock statements at the latest three months, it becomes ‘irregular’ that later becomes non performing asset after 90 days.

- If a bank didn’t show an account renewal or documents available for renewal of an account, then it becomes NPA if not renewed within 180 days.

- An out-of-order debit/credit account has an outstanding excess balance in the principal operating account without credit for more than 90 days. These accounts fall under the category of an NPA.

Also Read: How to remain financially sound in 2022

Categories of NPA

According to RBI, banks should categorise NPAs under one of the following:

Standard Assets

They are the non performing assets that are past due for anywhere between 90 days to 12 months, with a normal risk level.

Sub-Standard Assets

Effective from 31 March 2001, any asset that remains as NPA for less than or equal to 12 months falls under the category of sub-standard assets. In such cases, the security can’t ensure the recovery of dues to the bank.

Doubtful Assets

A doubtful asset is an asset that remains as NPA for more than 12 months. Based on currently known facts, the condition and value are highly questionable.

Loss Assets

When a bank or auditor identifies a loss associated with an asset which is not collectable comes under the category of a loss asset. These assets may have little recovery value but can’t warranty the bankable conditions.

Also Read: Golden Rules of Accounting

When Do Assets Become Non-Performing Assets?

In 2007, RBI defined Non-Performing Assets as an asset (including a leased asset) that becomes non-performing when it no longer generates income for the bank. Any loan or advance can become NPA when it is overdue for more than 90 days.

Example of a NPA

Let’s assume that a company takes a loan of ₹2 crores but fails to pay the ₹1,00,000 monthly interest for three consecutive months. The lender list this loan as an NPA on its balance sheet. The company will remain an NPA even if it pays the interests but fails to pay the principal amount at maturity.

Impact of nPA

Following are the impacts when an asset becomes a non performing asset:

- Impacts the economy because the banks lack sufficient funding for other development projects.

- Reduction in new investments could result in a rise in unemployment.

- In order to keep a profit margin, banks have to raise interest rates.

Also Read: Difference between Cash & Accrual Accounting

How Can Non-Performing Assets be Reduced?

There is a recovery mechanism to reduce NPA to restore the financial assets. The three main aspects of recovery are:

- Lok Adalat: A conflict resolution system to recover small loans of less than 5 lakh

- Data Recovery Tribunals (DRT): Recovery option for financial institutions to collect debts of ten lakhs or more.

- SARFAESI Act: Give banks an option to deal with NPAs without going to the courts, such as asset reconstruction, security enforcement and securitisation. It deals with the unpaid amount of loans of more than 1 lakh.

Stay in touch with latest taxation updates by following TaxHelpdesk on Facebook, Instagram, LinkedIn, and Twitter.

Disclaimer: Views of the author are personal.